Summary

- Microsoft's stock has been a big winner of the pandemic, and there may be one more 10-15% push higher on the way.

- The options market appears to be betting that the stock climbs over $320 by the middle of November.

- However, the stock's valuation is high on a historical basis and growth is about to slow considerably, giving the shares a path higher up until the next earnings report.

Microsoft (MSFT) has been a big winner of the pandemic, with the stock rocketing higher over the past 18 months. There are now signs the stock's advance may not be over, with bigger gains to come. The stock could be heading to around $320 to $325 over the next couple of months, nearly 10% to 15% higher than its price of roughly $293 on August 17, based on an analysis of the options market and technical charts.

The positive outlook for the stock comes despite the shares trading at a lofty valuation, just as earnings growth is expected to slow dramatically. It leaves investors in an awkward spot, wondering if they should continue to chase the stock higher just as year-over-year comparables get harder. But the reality of slowing growth may not hit until the company reports its next round of results in late October, giving the shares a path higher over the next couple of months.

Slower Growth

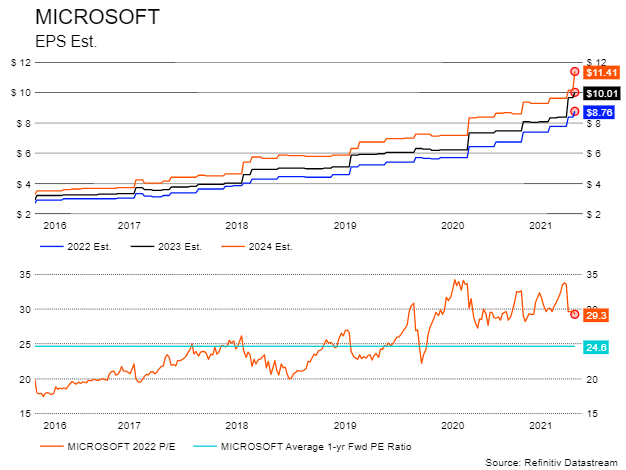

Earnings growth for Microsoft is expected to slip going forward, rising by 8.8% in the fiscal year 2022 from 39.7% in fiscal 2021. It is forecast to accelerate in the fiscal year 2023, but only to 14.3%, which is still slower than its earnings growth of 22.4% and 21.3% in 2019 and 2020. Additionally, growth rates over the next four quarters are expected to decelerate, dropping to 7.5% by the fourth quarter from 13.5% in the fiscal first quarter.

The slowing growth rate presents the biggest problem for the stock because it currently trades at 29.3 times 2023 earnings estimates. This is not a cheap valuation for Microsoft. In fact, over the past 5 years, the stock has averaged a PE ratio of just 24.6, making the current valuation very pricey on a historical basis.

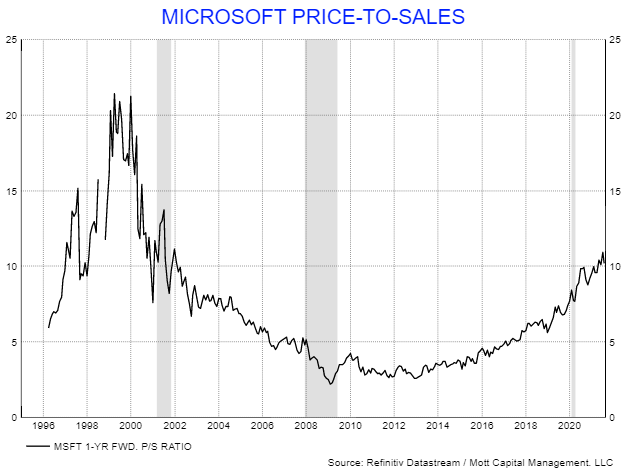

On a price-to-sales metric, the stock has only been more expensive one other time, which was in the late 1990s and early 2000s during the dot.com mania. This could really leave an investor feeling confused, with an extremely high valuation for a sales multiple, and while the PE ratio is high, but tolerable. However, the price-to-sales metric is essentially off the charts at current levels.

Options Outlook

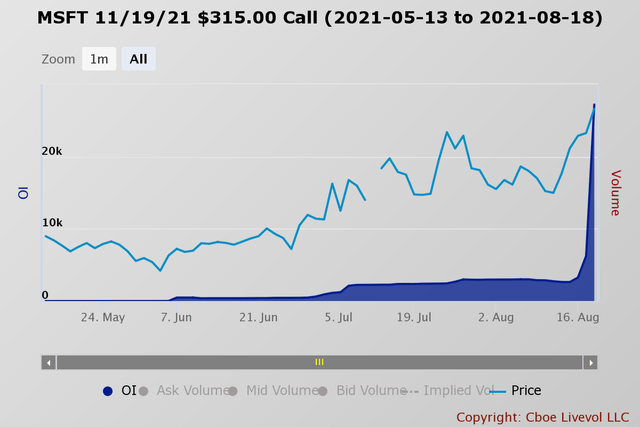

Still, the questionably high valuation isn't stopping the options market from being very bullish on the stock. Perhaps that is because of the stock's momentum behind it since the start of the pandemic. On August 18, the open interest for the November 19 $315 calls rose by around 20,000 contracts. The data shows the call options were bought for roughly $4.50 to $4.75 per contract. It implies that the stock is trading at $319.75 or higher by the expiration date, a gain of around 9.1% from its closing price on August 17. It is a massively bullish bet as well, with premiums paid off roughly $9.5 million.

Technicals Support A Move Higher

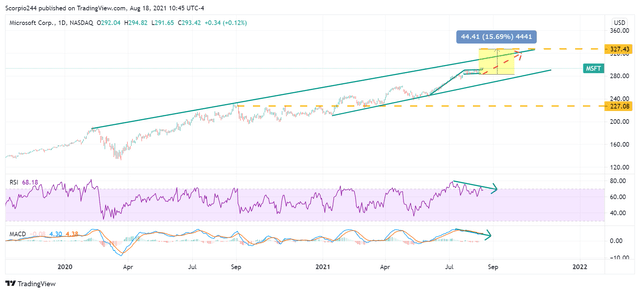

From a technical perspective, the stock may have further to climb after breaking out of a bullish flag pattern when it rose above resistance at $290. The pattern formed starting around June 4 and a projection of the move off of that starting pointing suggests the stock rises to around $327 over the next few months a gain of about 15%, which is roughly in line with the bullish options bet placed.

The one concern here is that this could prove to be the final push higher for Microsoft, as there is a bearish divergence currently forming between the stock's price and the momentum indicators. The relative strength index and the MACD are slowly trending lower, and this would indicate that momentum in the stock is now waning and bearish momentum is taking hold.

The current options and technical setup would suggest the stock is likely to flourish for some time longer, while the fundamentals would suggest the valuation is stretched. Overall, it seems to give Microsoft a path higher at least until the next round of earnings, which is likely not to come until sometime in late October.

精彩评论