CNBC’s Jim Cramer feels the urge to sell ROKU. MavenFlix talks about some of the key reasons why the TV personality may be right.

Roku stock has tanked from $274 per share in mid-November to around $225 now. The market had been projecting high revenues in the most recent quarter, but Roku did not deliverthe expected results earlier this month.

Reinforcing bearishness, Jim Cramer has recentlysaidon CNBC: "every time I look at Roku, I want to sell it". The comment followed the presenter’s take on a sell-side report that recommended selling the stock. But why such skepticism?

Roku as a dominant platform

Regarding streaming platform aggregators, Roku stands out as the most used and the best known. However, it may still be too early to say that the company will continue to dominate this market. Roku could face increasing competitive pressures, especially against Amazon. The e-commerce and cloud giant sells Fire TV systems and is also expected to start producing smart TVs to compete directly with the San Jose-based company.

High multiples to go with disappointing revenues

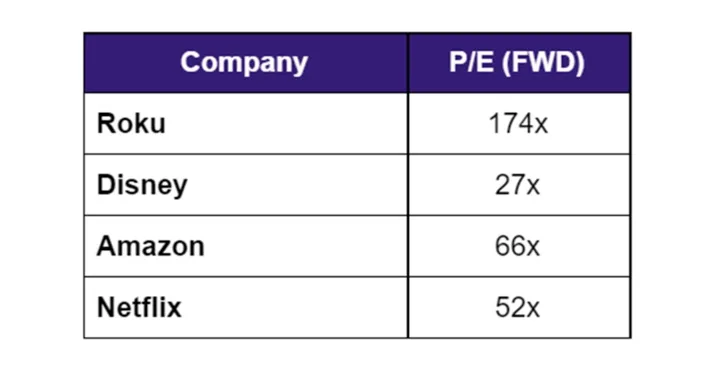

Roku is trading at a P/E that is almost three times higher than its peers’. One would need to fast-forward three years to find a 2024 earnings multiple of 50 times more palatable, even if not overly de-risked yet. Investors with a GARP (growth at reasonable price) mindset might be tempted to consider investing in other companies, including Disney and Netflix, which carry substantially lower multiples.

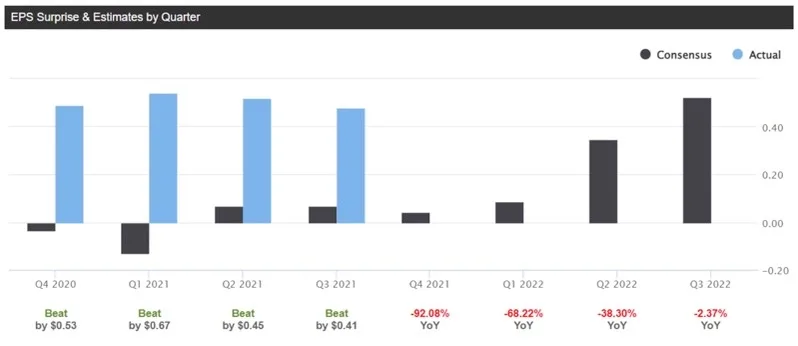

ROKU’s sky-high valuations could be justified by outsized growth opportunities. In recent quarters, the company has delivered higher-than-expected earnings, and expectations for longer-term bottom-line performance has been sloping higher as well. See below.

However, projections for next year are all below 2020 and 2021 numbers, which means that the market expects a slowdown in the company's growth pace. This could be a warning sign for investors in the short term, as more modest profit growth can translate into valuation compression for ROKU.

Faceoff against competitors

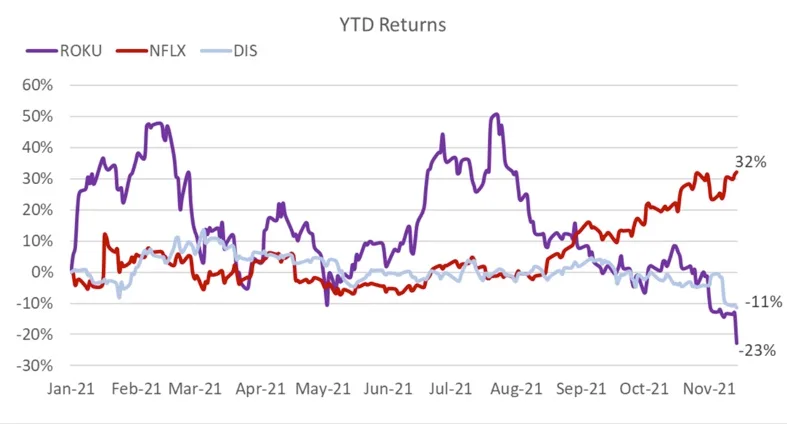

Compared to its main peers, ROKU stock has been performing poorly. Even DIS, a 2021 loser in the large-cap tech and media spaces, has done substantially better at a year-to-date loss of 11% (see below) while ROKU has fallen by more than 20%. At the same time, Netflix has accumulated gains of 32%. Clearly, momentum has been on the side of the Los Gatos company.

Some investors could see ROKU’s underperformance as a buying opportunity. The argument loses strength, however, when P/E still looks so bloated.

Our view

Even though analysts that cover ROKU have high expectations for the long term, we think that there are better stocks to play the streaming sector's growth opportunities. While ROKU can grow earnings into its rich valuations, we fear for short-term headwinds (e.g. negative momentum, growth deceleration, etc.) and see companies like Netflix, Disney and Amazon as better bets.

精彩评论