Summary

- While most semiconductor stocks have been enjoying a nice rally this year, Intel was apparently not invited to the party.

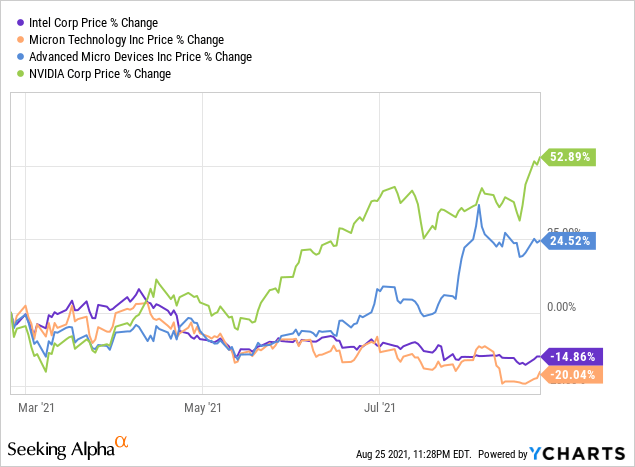

- During the past six months, Intel is actually down 15%.

- The question remains whether or not the stock is a value trap or a coiled spring ready to pop.

Just as industrial giants like Ford Motor Co. (F), Caterpillar (CAT), and 3M Co. (MMM) propelled the U.S. (and the world) forward in the early 20th Century with major industrial innovations, the semiconductor manufacturers are driving the technology revolution of the 21st Century.

It seems like chips are needed in everything these days,andthe pressure is on to make things faster, smaller, and cheaper.

That said, while most semiconductor stocks have been enjoying a nice rally this year (for good reason),IntelCorp. (INTC) was apparently not invited to the party (or maybe it's just late?).

As shown in the chart below, the bifurcation between the winners and the losers in the space has become quite clear over the past 6 months. Chip darlings like NVIDIA Corp. (NVDA) and Advanced Micro Devices (AMD) are up 52.9% and 24.5%, respectively.

Meanwhile, Intel is down 14.9% and Micron Technology (MU) is down over 20%!

While we have recently penned our thoughts about Micron,NVIDIA, and Advanced Micro Devices, it's time to dig deeper into Intel too.

To be fair, Intel has had its fair share of challenges this year,despitegeneral tailwinds in the industry (i.e., chip demand far outpacing supply).

Specifically, Intel has had some well-documented manufacturing blunders that have caused major delays (and loss of some market share). This has triggered concern amongst investors that the stock may be a potential "value trap" now.

All that said, I'm definitely in the camp that believes that this industry veteran could still be a coiled spring ready to pop with potential to close the gap with some of the winners (like NVDA and AMD).

Personally, I don't think we are anywhere near peak demand for chips and I believe that Intel's fabrication capabilities are (and will continue to be) a huge advantage for the company for years to come.

The rest of this article will take a quantitative look at Intel to confirm my qualitative assumptions that the stock should be trading higher from here:

- Long-Term Thesis (Dividend, Safety, Value)

- Short-Term Thesis (Strike Zone, EPS Risk, Technical Support)

- Upside Target

- Cash-Secured Put Analysis (Premium Yield, Margin-of-Safety, Delta)

- Downside Considerations

- Conclusion

Sources for all data and tables below: Option Income Advisor and YCharts

Intel Corp.

Sector/Industry: Technology / Semiconductors

Intel is the world's largest chipmaker. It designs and manufactures microprocessors for the global personal computer and data center markets. Intel pioneered the x86 architecture for microprocessors. It was the prime proponent of Moore's Law for advances in semiconductor manufacturing, though the firm has recently faced manufacturing delays. While Intel's server processor business has benefited from the shift to the cloud, the firm has also been expanding into new adjacencies as the personal computer market has stagnated. These include areas such as the Internet of Things, artificial intelligence, and automotive. Intel has been active on the merger and acquisitions front, acquiring Altera, Mobileye, and Habana Labs in order to bolster these efforts in non-PC arenas. (Source: YCharts )

Long-Term Thesis (Dividend, Safety, Value)

In general, our high-level long-term investment thesis on a stock is more quantitative in nature than qualitative.

That said, Intel currently ranks very well across our key long-term ranking measures: Dividend (7), Safety (8), Value (10)

Dividend

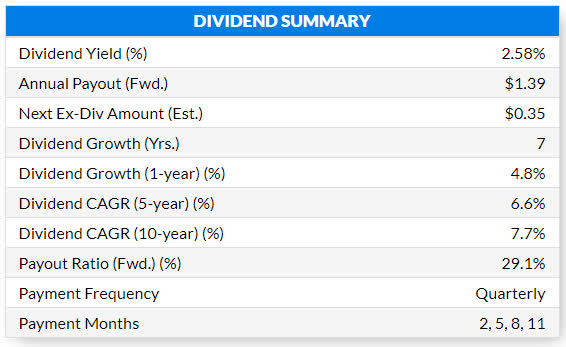

Intel has raised its dividend in each of the past seven years and currently yields 2.6% with a reasonably low payout ratio of 29.1%.

In addition, the company has steadily been growing its annual payout, with 1-year, 5-year, and 10-year compound annual growth rates of 4.8%, 6.6%, and 7.7%, respectively.

Safety

Up until 2020, Intel had experienced relatively stable sales and EPS growth. However, manufacturing delays over the past year or so have caused sales and EPS to dip. Management does expect operations to stabilize in 2022 and 2023.

That said, the company's balance sheet remains strong with $25 billion of cash/short-term investments and management is producing a solid return on invested capital of 16%.

Intel's low historical stock volatility, with a five-year standard deviation of 29% and a beta of 0.60, is also adding to its relatively high Safety Ranking.

Valuation

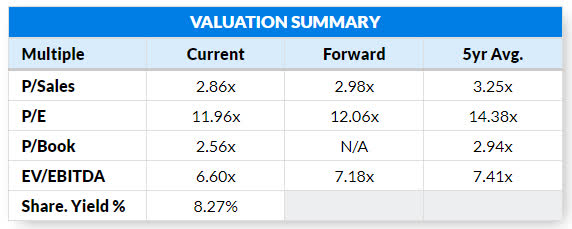

Intel currently carries our top rating of 10 for valuation. As shown in the table below, the company is trading at a discount compared to its historical averages across all 4 valuation multiples we look at.

Intel also has a very attractive shareholder yield of 8.3%.Note that shareholder yield is the combination of buyback yield and dividend yield.

Long-Term View

Based on the data above and our various rankings, we have a Bullish long-term perspective on Intel. Although sales and EPS are just starting to stabilize from the recent dip, the company's valuation and volatility profile are very attractive.

Short-Term Thesis (Strike Zone, EPS Risk, Technical Support)

From a short-term perspective (especially as it's related to selling cash-secured puts), estimating a good "strike zone" is key to our analysis. Our strike zone takes into account (1) the stock's volatility, (2) recent performance (i.e., how much has it already pulled back from its recent highs), (3) near-term EPS risk, and (4) the overall volatility of the market (i.e., VIX level).

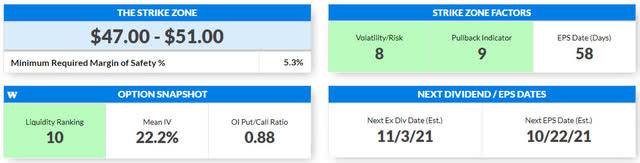

As shown in the table below, our strike zone for Intel currently is $47.00-$51.00, representing a required minimum margin of safety of 5.3%.

As discussed in the safety ranking analysis above, Intel ranks positively on a relative basis for stock Volatility/Risk. In addition, the stock has already pulled back over 21% from its recent high (so its Pullback Indicator also ranks positively). Both of these strike zone factors help keep the minimum required margin of safety at a reasonable level of 5.3%.

Also, Intel's next EPS announcement is 58 days out, so we won't have any EPS risk to worry about in the near term.

As shown in the chart below, the stock's uptrend has been broken with shares trading below both the 50-day moving average (blue line) and the 200-day moving average (red line). That said, we think the stock could have put in a short-term bottom around $52.00 a few days ago and we would look for that level to hold as support.

Short-Term View

There appears to be some decent technical support around the high end of our strike zone of $47.00-$51.00,whichobviously makes us feel relatively good about holding the stock and potentially selling additional cash-secured puts in the strike zone if we can.

Upside Considerations (Target Price)

Despite 26 of the 42 Wall Street analysts having a "Hold" rating or lower on the stock, the consensus price target for Intel is still $63.00 (representing over 17% upside from current levels).

Also, with so many analysts currently at "Hold" or below, it opens the door for a flurry of upgrades in the future (which typically come with price target hikes as well). This catalyst could be significant.

That said, we also think that there's definitely some room for margin expansion for Intel in the short term as the company's earnings stabilize.

If you put just a 15x multiple on forward earnings of $4.50 per share, that would equate to a $67.50 stock price (representing over 25% upside from current levels).

Cash-Secured Put Analysis (Premium Yield, Margin-of-Safety, Delta)

Although we already own the stock, we think that now is a good time to potentially add to our position and ride the upside.

For new investors, we think the stock is really attractive at current levels and would recommend it as a buy.

We primarily trade an income strategy that we call the Triple Income Wheel, which starts with writing cash-secured puts on high-quality stocks that you would like to own at a lower price. We won't go into full detail here, but the diagram below is a good summary of the strategy.

Ideally, when we sell a cash-secured put and start the Triple Income Wheel process, our put is in our "Strike Zone" for that stock. In our opinion, that puts the odds of long-term success in our favor.

The three main data points we look at when analyzing a cash-secured put trade are:

- Premium Yield% (or Average Monthly Yield%): Measure of expected return on capital assuming that the option expires worthless (out-of-the-money).Assumes that the option is fully cash secured.

- Margin-of-Safety %: Measure of downside protection or the percentage that the underlying stock could decline and would still allow you to break even on the option trade.

- Delta: A good proxy for the probability that the put option will finish in-the-money.

Note that there's always a negative correlation between Premium Yield and Margin of Safety: The higher the Premium Yield for a given strike month, the lower the Margin of Safety.

An investor always should be honest with themselves about their risk tolerance. The Triple Income Wheel can be adapted to suit your needs.

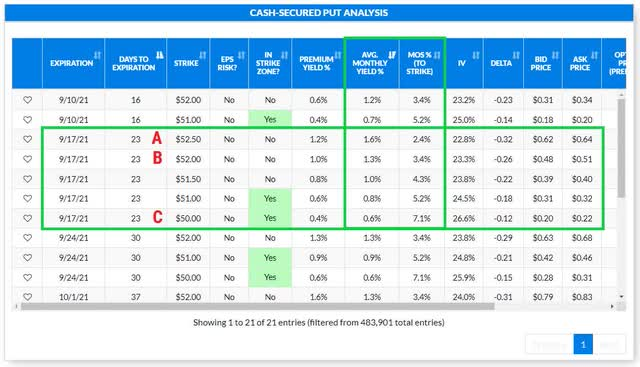

Now let's look at the cash-secured put analysis for Intel. We're focused on the September monthly contract that expires on 9/17/21.

We have highlighted three levels of trades based on various risk profiles: Aggressive (-A-), Base (-B-), and Conservative (-C-).Please listen to the video above for further details.

Ideally, we like to stick with our target levels for our Base portfolio:

- Average Monthly Yield % (AMY%): 1.0%-1.5%

- Strike price that is in the strike zone (i.e., margin of safety above the required minimum)

- Delta < 30

The INTC Sept 17th $52.00 put option @ ~$0.50 meets all of our criteria with an AMY% of 1.3%, a Margin-of-Safety of 3.4%, and a Delta of 26.

Again, based on your risk tolerance, you could choose a strike price that is more aggressive ($52.50 strike) or more conservative ($50.00 strike) than the base trade.

Downside Considerations

Assuming we sold the INTC Sept 17th $52.00 strike put option @ $0.50, we would collect $50.00 of premium for each option contract sold. In return for this premium, we agree (and are obligated) to buy 100 shares of INTC stock for each contract sold at the strike price of $52.00.

If the stock stays above $52.00 between now and expiration (9/17/21), the option expires worthless and we keep the premium of $0.50.

However,the downside of this trade comes into play if the stock closes below $52.00 on expiration (9/17/21). Since we're obligated to buy the stock at $52.00, we would have a potential unrealized capital loss on our hands (depending on how low the stock closed on expiration). We do get to keep the premium either way though, so our breakeven cost basis would be $51.50 ($52.00 - $0.50).

All that said, when managing the Triple Income Wheel, you should expect to take assignment (buy the stock) on 5%-10% of your cash-secured put trades.

But when this happens, we get to move to step 3 in the diagram above and sell some covered calls on our stock position to start the income flowing again and start mitigating our risk right away.

Conclusion

Based on our long-term and short-term views on Intel, we believe that the stock is a good buy at current levels,butit's even a bigger win if you can add to your Intel position with a cost basis of $51.50 (and sit back and collect the dividend as the stock rises).

精彩评论