Summary

- PayPal's Q3 2021 guidance took investors by surprise.

- PayPal contends that asides from eBay Marketplace's migration off PayPal, its underlying business is performing very strongly.

- PayPal is priced at 13x sales. This is very attractively priced for such an entrenched high-quality payment solution platform.

Investment Thesis

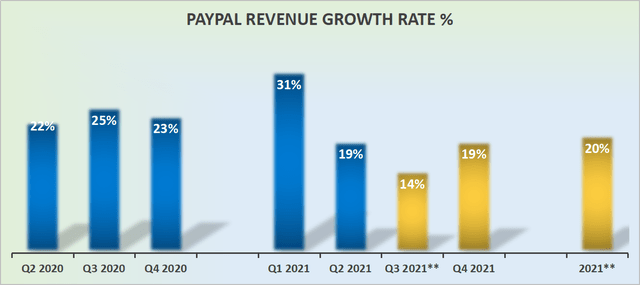

PayPal's (PYPL) guidance for Q3 is pointing towards a marked deceleration where its revenues are expected to grow approximately 14% y/y. However, this is predominantly due to eBay (EBAY) Marketplace exiting PayPal's platform.

For context, this will be a meaningful headwind of approximately 850 basis points during Q3, and it will slowly reduce its impact during Q4 2021.

However, putting aside eBay's impact, PayPal's core operations remain strong and PayPal is still expected to grow by 20% this year,includinge Bay's headwind.

What's more, PayPal is expected to bring in $5 billion of free cash flow this year, putting the stock trading at 74x free cash flow.

In short, investors have no reason to be dissatisfied with this quarter's performance. PayPal is an attractive investment opportunity.

Investor Sentiment Going Into Earnings

As you can see above, contrary to countless other fast-growing names, PayPal had actually had a very strong run-up in its shares since May.

Hence, given this backdrop where investors had such high expectations from PayPal, any mishap during the quarter was obviously going to take the share price down.

Now, let's get into its results.

Revenue Growth Rates Slow Down, With a But

The big takeaway is that PayPal is reaffirming its guidance for 20% y/y in 2021. Having said that, the elephant in the room is that Q2 2021 saw just 19% y/y revenue growth rates.

Given that during Q1 its revenue had just grown by its fastest rate in PayPal's history, investors were minimally expecting PayPal to continue that momentum and shine this quarter. After all, this is a company that has a long history of delivering positive results and easily beating its guidance.

At the core of the after-hours reaction, we have to keep in mind that this is a company that buy-and-hold investors perceived as ''safe'' and one that ''shouldn't'' have negative surprises.

Hence, this rare weak quarter is more likely than not to be met by not only heavy selling in the coming days, and I fully suspect that the media will all over this stock reporting how PayPal has lost its flow.

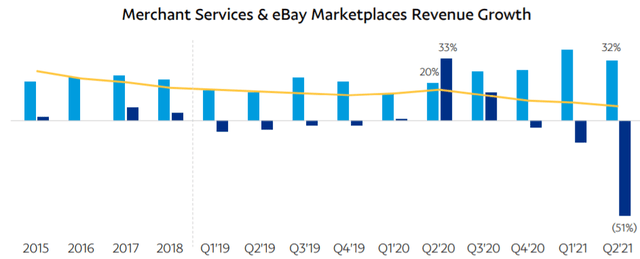

PayPal's CEO Dan Schulman points out that eBay was a headwind for PayPal during the quarter as eBay Marketplaces stopped being served by PayPal.

What's more, PayPal declares that eBay Marketplaces accounted for roughly 8% revenue growth rate headwind, which is particularly noticeable given the strong performance in the same period a year ago.

This is what PayPal's CFO John Rainey said during the call:

So last year in the second quarter, we grew revenue 22%, and in that number, there was a benefit of 5 percentage points of growth from eBay. So 22% revenue growth for 5 percentage points of benefit from eBay. This year in the second quarter, we grew revenue 19% and that number included 800 or 8 percentage points of headwind related to eBay's business.

Looking ahead, PayPal highlighted during the call that by year-end, eBay's total payment volume (''TPV'') will account for just 2.5% of PayPal TPV by year-end.

What's more, during Q2 2021, putting aside eBay's headwind, PayPal's revenue would have been up 32% y/y. Given that eBay will have migrated to its own payment solutions by Q4 2021, investors won't have to be patient too long until PayPal is once again reporting strong revenue growth rates.

Indeed, asides from eBay there's a lot to be attracted to here.

PayPal's Diverse Product Portfolio in 2021

The biggest launch during the quarter was Zettle in the U.S. This is a digital point-of-sale card payment solution. Although it arrives into a very crowded space arguably a little late in the game.

Having said that, Venmo was also a latecomer to the digital wallet space and that hasn't stopped Venmo's performance in Q2 2021 growing its total payment volume by 58% y/y to $58 billion. This translated into Venmo increasing its revenues by 70% y/y.

Venmo's performance during Q2 2021 was driven by robust crypto trading on the platform.

Also, PayPal's Buy Now, Pay Later is resonating with consumers and merchants with momentum accelerating sequentially from Q1 2021 to Q2 by 50%.

Altogether, despite investing in different products launches, PayPal still generates strong free cash flows.

PayPal is a Free Cash Flow Machine

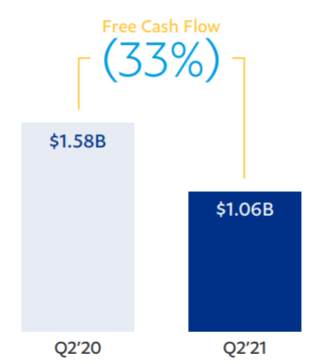

During Q2 2021, PayPal's free cash flow was down 33% y/y to $1 billion. Obviously, when taken together with its lackluster top-line growth rate during Q2 2021 this doesn't paint a particularly impressive picture of PayPal's performance.

On the other hand, consistent with its previous two quarters, PayPal once more reaffirmed its free cash flow guidance for $5 billion in 2021. Demonstrating that aside from the impact of eBay's migration, PayPal's free cash flow performance in 2021 remains unchanged from the start of the year.

Valuation - Not Expensively Valued

High-quality stocks rarely come cheaply towards the end of a very long bull market.

In a market where many companies are highly unprofitable and with middle-of-the-road revenue growth rates, PayPal is not only growing by 20% CAGR this year, but it's expected to grow at an even faster ratenext year, while also generating ample free cash flow.

There aren't too many companies out there as entrenched as PayPal in fintech priced at 74x free cash flow.

On the surface, this may appear expensive, but readers should keep in mind that this is free cash flows and not a sales multiple.

Meanwhile, for context, on a sales multiple, PayPal trades at 13x sales.

The Bottom Line

PayPal's Q3 guidance took many investors by surprise, particularly given that this blue-chip household name rarely misfires. However, its underlying performance remains very strong.

Given its strong free cash flow generation, and approximately mid-20s% CAGR expected next year, I believe that this stock is cheaply valued at just 13x sales.

However, since there are so many high-growth small-cap stocks that are now heavily into correction territory, I believe that there are even better investment opportunities elsewhere.

精彩评论