Summary

- The infrastructure bill signed by President Joe Biden will deliver at least $20.5B for the clean energy sector.

- Another $1.75T reconciliation federal bill includes over $550B for multiple clean energy projects, such as carbon capture and green hydrogen technologies.

- PLUG and BE reported impressive revenue growth in the past four years.

- We discuss which is the better buy now.

Investment Thesis

The $1.2T infrastructure bill signed by President Joe Biden is expected to deliver massive tailwinds to the clean energy sector. Both companies have displayed remarkable growth in the past four years, with Plug Power Inc. (PLUG) growing at a CAGR of 42.41% and Bloom Energy Corporation (BE) at a CAGR of 33.34%. While PLUG seems to lead the pack for green hydrogen technology, BE is catching up with its low-cost green hydrogen in its collaboration with Heliogen, Inc.

We discuss which stock is the better buy now.

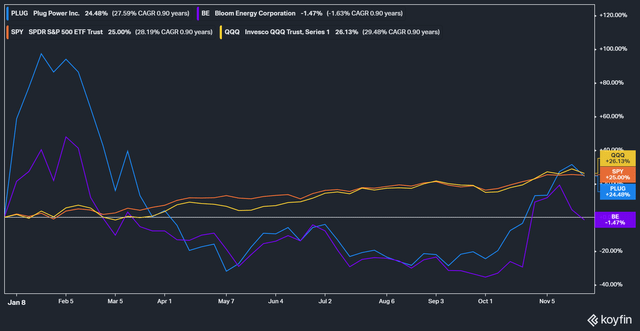

Stock YTD Performance

Both stocks started the year with tremendous excitement. PLUG stock quickly raced to a YTD gain of more than 100%, while BE stock followed closely. However, both stocks were severely battered during the rotation to high-quality stocks in February. As a result, not only did their momentum disappear, but it also turned bearish abruptly. PLUG and BE stock found themselves underwater by April and stayed in the red over the next six months. However, the recent infrastructure bill lifted investors' spirits and confidence in both stocks. As a result, their momentum has significantly recovered. PLUG stock recovered remarkably, and the stock is just slightly underperforming the market with a YTD gain of 24.5%. In addition, BE stock is near getting out of the trenches with a YTD return of -1.5%.

Infrastructure Bill Is A Significant Boost To Clean Energy Companies

The infrastructure bill signed on 15th November 2021 delivered a massive boost to many sectors, including clean energy. The benefits to the clean energy sector include:

- $8B to develop regional clean hydrogen hubs. It includes $500M for clean hydrogen manufacturing and $1B to decrease the cost of clean hydrogen production from electrolyzers.

- $7.5B to develop electric vehicle charging infrastructure and vehicle-to-grid infrastructure.

- $5B to develop zero- and low-emission buses and ferries.

- Part of the $17 billion in port infrastructure and $25 billion in airports will also be used to develop low-carbon technologies.

On top of the $1.2T signed infrastructure bill, a separate $1.75T reconciliation bill is currently in consideration. This bill includes over$550B for multiple clean energy projects, including carbon capture and green hydrogen technologies. These will help to accelerate the research and development while lowering the cost price for green hydrogen. As a result, it will help promote the adoption of green hydrogen as alternative energy by most in the commercial and industrial sectors.

Multiple giants in the industrial sector such as Phillips 66 (NYSE:PSX), Airbus (OTCPK:EADSF), and SK Group have already signed various collaborations with PLUG and BE to reduce their greenhouse emission by 2030. In addition, a few US states have also embraced clean energy initiatives, such as California,Washington, and Hawaii. For example, in 2019, California set a target of 60% renewable energy on the grid by 2030, with a goal of 100% climate-friendly energy. These include green hydrogen on top of hydroelectricity and nuclear power.

As a result, it is not hard to see that green hydrogen could experience massive growth and fulfill its potential moving forward. The annual use of hydrogen is expected to grow from 115M metric tonnes to 800M metric tonnes by 2050. It will account for almost 20% of total global energy consumption by then.McKinsey & Company also estimated $150B would be spent in 2021 for hydrogen-related projects globally.

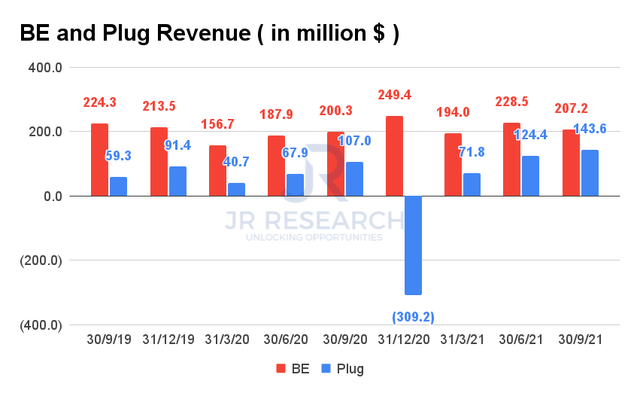

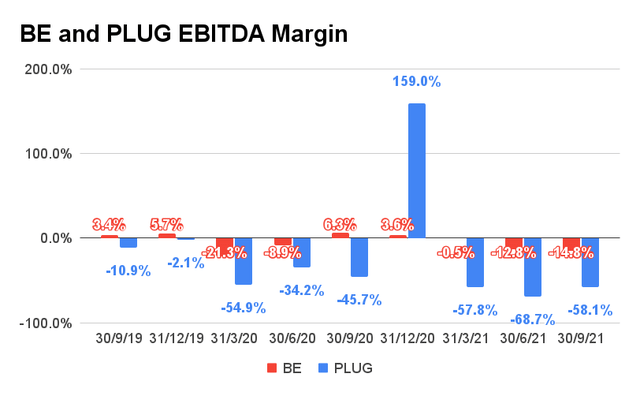

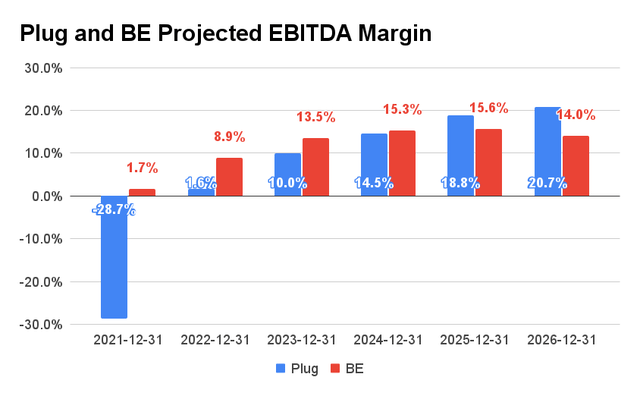

PLUG reported impressive revenue growth in the past four years, at a CAGR of 42.41%, while BE recorded a CAGR of 33.34%. In FQ3'21, PLUG reported a 15.4% QoQ increase in revenue, while BE reported a 9.3% QoQ decline. However, BE has delivered a more consistent EBITDA margin at an average of -5% over the past two years. In contrast, PLUG has shown much greater volatility in its profitability profile. The relatively weak profitability of both companies is mainly attributed to significant R&D work in the green hydrogen market. PLUG also invested substantially in its electrolyzer manufacturing giga-factory, which was recently completed in November 2021. The company expects to ramp up its electrolyzer production by 10x and achieve scale efficiencies to drive down hydrogen costs meaningfully. As for BE, the company expects to produce the lowest cost green hydrogen through its breakthrough electrolyzer technology in collaboration with Heliogen, Inc.

BE Is One Of The Market Leaders In Low-Cost Green Hydrogen

In July 2021,BE and Heliogen, In cannounced their collaborations to produce green hydrogen using the combined technology of Heliogen's concentrated solar energy system and the Bloom Electrolyzer. As of November 2021, the partnership led to a successful demonstration in Lancaster, California. The combined technology has shown promise for the mass production of low-cost green hydrogen. Bloom Energy Chief Technology Officer Venkat Venkataraman said:

This integration with Heliogen underscores the value that strategic collaborations and industry-leading innovation can bring to driving change and making positive impacts for our climate. With a focus on providing highly efficient and low-cost green hydrogen at scale, we will be a leader in low-cost hydrogen. (Bloom Energy)

Compared to the conventional Proton Exchange Membrane (PEM) technology using electricity, BE reported that its new combined technology with Heliogen can produce green hydrogen with 45% cost efficiency. BE highlighted that electricity accounts for almost 80% of the cost of green hydrogen. With the use of steam through Heliogen's concentrated solar technology, BE expects to reduce production costs substantially. In turn, it will encourage the mass adoption of its clean energy products. It's because the commercial and industrial sector is responsible for more than a third of global energy consumption and a quarter of global CO2 emissions. BE is working towards replacing fossil fuels in widespread commercial and industrial applications.

Both Companies Are Expected To Grow Rapidly

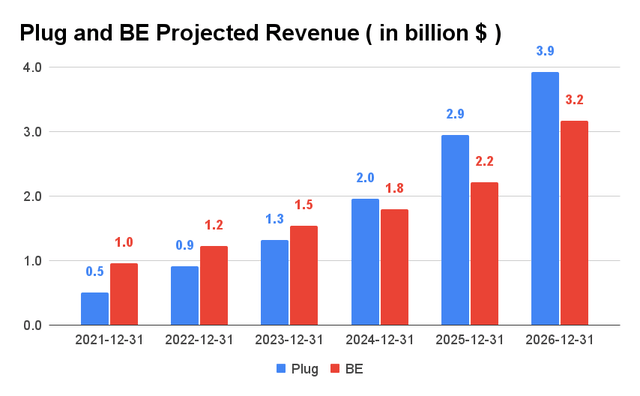

Both companies are expected to report significant revenue growth. PLUG is estimated to post a higher revenue CAGR of 50.81%, compared to BE's revenue CAGR of 26.19%. PLUG is also expected to post higher average EBITDA margins over the next five years.

Nevertheless, if BE can successfully commercialize its applications, we expect BE's estimates to be revised upwards. If we consider BE's electrolyzer efficiency of 45%, BE's green hydrogen cost could potentially rival PLUG's target of $1.5 per kg. Currently, the estimated price in October 2021 for green hydrogen is within the range of $3.18 and $5.75 per kg. Therefore, the potential for both companies could be massive if they are successful in their commercialization initiatives.

Which Stock Is The Better Buy Now?

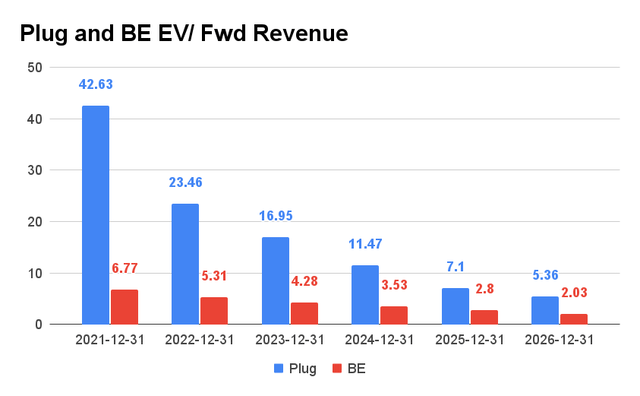

PLUG is currently trading at an EV/NTM revenue of 26.7x. It's lower than its peers' comps set mean of 36.09x. Notably, it is significantly higher than BE's 5.2x. Nevertheless, we think there's a considerable amount of growth premium embedded into their current valuation, and more so for PLUG.

But, if we observe their EV/Fwd Revenue valuation trend, both companies are expected to grow rapidly. Therefore, if investors are willing to pore over their valuation with a speculative lens, their premium might be justified.

We believe that PLUG will be the leader in its field. Moreover, the market also thinks likewise as reflected in its valuation. Nevertheless, BE attracts a much lower premium. PLUG has demonstrated strong leadership and is also expected to grow faster, so we prefer PLUG stock over BE stock.

Therefore, werate PLUG at Buy for speculative investors only.