Summary

- Okta is rapidly growing its top line and guides investors for at least 35% CAGR over the next 4 years.

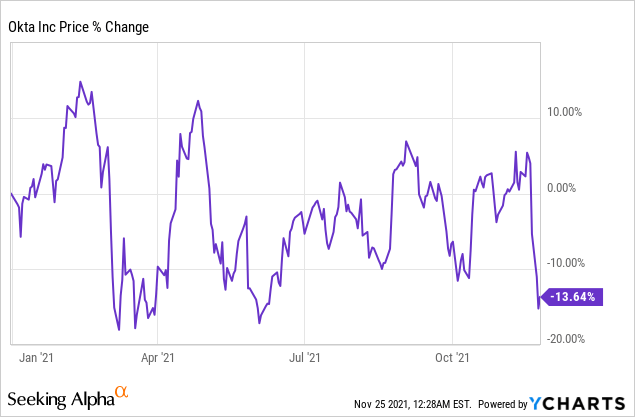

- However, its shares are in negative territory this year, underperforming many high flying peers.

- Investors considering this investment, at just 20x forward sales, this is the best entry point for a while now.

Investment Thesis

Okta (OKTA) is an Identity Management platform. It's rapidly growing and declares to investors that it's going to grow its revenues by at least 35% CAGR to $4 billion over the next 4 years.

Right now, its valuation is the most enticing it has been for a while, and for investors seeking this investment, this is perhaps the most rewarding time to consider these shares in a while. At 20x forward sales, investors will struggle to get Okta much cheaper.

Investors' Sentiment Has Been Choppy

Back in 2020, Okta was a business that could do no wrong. Investors were passionately clamoring for the stock. But this year, very few investors would have had the stamina to withstand this volatility.

Incidentally, back in July, Istated,

[...] Given that Okta's stock is already priced at 32x forward sales, new investors to the stock will struggle to find enough of an edge that's not already priced into its stock.

And despite a choppy trajectory, since July the stock has seen its multiple compresses, making it now an interesting investment opportunity.

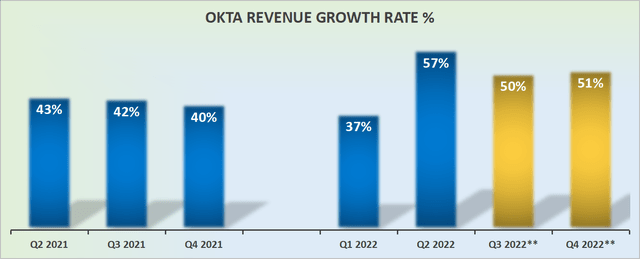

Okta's Revenue Growth Rates Remain Impressive

On the surface, these growth rates and guidance display an impressive growth trajectory for Okta.

That being said, its Q2 2022 results included Auth0, Okta's large acquisition. Without this acquisition, the stand-alone business grew by 39% y/y.

Thus, investors haven't been as compelled towards Okta, as there are some doubts over whether or not Okta is going to continue growing at such fast rates going forward.

For their part, Okta's management team consistently reassures investors that Okta will grow at a CAGR of at least 35% over the next 4 years to $4 billion in revenues.

Moreover, Okta's normalized billings in the quarter for its stand-alone business was up 47% y/y. This should ease investors' concerns over whether or not Okta is in fact capable of growing at 35% CAGR.

Indeed, as you know, billings are a leading indicator of a company's revenue growth rates. In the ideal scenario, you want to see billings coming in slightly higher than its revenue growth rates, but if that's not the case, you'd still hope to see them coming in higher than its long-term revenue growth target of 35% CAGR.

So, let's understand the opportunity here some more.

Why Okta? Why Now?

Okta allows secure access to devices and enables users to use technology safely. By identifying users, Okta secures users and connects them to the right technology.

As you can see above, both Okta and Okta (Auth0), Okta's acquisition, have both been recognized as leaders by Gartner.

Furthermore, as you can see, the number of customers rapidly adopting Okta's platform, with customers spending more than $100K of annual contract value (''ACV''), increased by55% y/y for fiscal Q2 2022.

Yes, there was a notable jump from its fiscal Q1 2022 quarter, where customers spending more than $100K of ACV were only up 31% y/y. A meaningful portion of that jump in Q2 2022 would have come from its Auth0 acquisition.

Nevertheless, the recent jump in customers didn't stop Okta's net retention rates from coming in at 124% for Q2.

In sum, the point to impress upon readers is that this company is without a doubt rapidly growing, even if its share price is in negative territory in 2021.

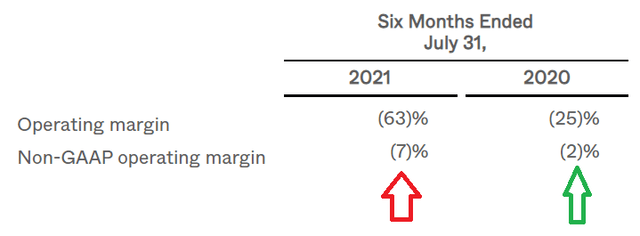

Bearish Consideration: Profitability Profile

As you can see above, despite rapidly growing its top-line at a fast rate, Okta isn't quite benefitting from strong operating leverage, as its non-GAAP operating margin points to negative 7% for H1 2022 compared with negative 2% in the same period a year ago.

Obviously, readers would rapidly retort that this is because of the Auth0 acquisition, and integrations the company has had to do.

On that front, I point readers to its guidance for the quarter ahead, where Okta's non-GAAP operating margins are expected to reach negative 10%. Thus, if last quarter the unappetizing profit margins were due to its acquisition of Auth0, what's the reason for its upcoming quarter to point to such lackluster profit margins?

OKTA Stock Valuation - Attractively Priced

Okta is now priced at 20x its fiscal 2023 revenues (ending January 2023).

If we look over its past twelve months, this is certainly towards the lower end of its multiple on a forward basis.

Compared with other hyper-growth companies, such as CrowdStrike (CRWD) that's priced at 27x forward sales, or MongoDB (MDB) at 31x forward sales, Okta is certainly attractive.

The Bottom Line

Investors that are interested in increasing their exposure to digital enabling platforms, Okta right now trades at the cheapest valuation it has been for some time.

The company continues to rapidly grow and appears to be successfully integrating its Auth0 acquisition.

What's more, Okta reassures investors that it can continue growing its revenues at 35% CAGR over the next 4 years, thus offering investors much craved visibility and strong growth prospects.

All that being said, given the plethora of stocks that have sold off in the past few weeks, I'm finding better investment opportunities elsewhere.