Summary

- NIO is one of the leading pure-play new electric vehicle makers in China.

- The company is estimated to grow rapidly, as it expands aggressively into Europe next year.

- We discuss what investors should expect moving ahead in 2022 and beyond.

- We also discuss whether investors should add NIO stock now.

Investment Thesis

NIO Inc. (NIO) is one of China's leading new electric vehicle (NEV) players. Despite almost going bankrupt a few years ago, the pure-play NEV player has made a tremendous comeback.

NIO posted weak October deliveries. Nonetheless, the company is still leading total deliveries YTD among its leading pure-play peers. The competition is very close, but NIO continues to grow rapidly. The scale and immense opportunities of the Chinese market made Elon Musk famously proclaim that China will be Tesla's (TSLA) largest factory and market.

Amid NIO stock's relatively weak performance in 2021 so far, we discuss whether it's time for investors to add the stock.

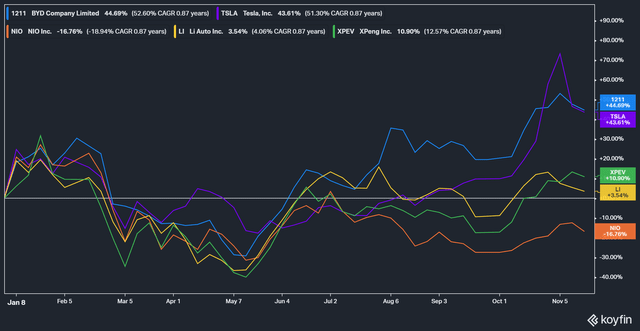

NIO Stock YTD Performance

NIO stock has had a subpar year in 2021. While it had started the year strongly, its upward momentum collapsed following the rotation from growth to value stock in February 2021. Despite making a remarkable recovery in May, it has remained in a consolidation phase. In contrast, its Chinese NEV peers have managed better performances so far. NIO stock is currently underperforming its leading Chinese NEV peers, and Tesla stock with a YTD return of -16.8%

NIO Operates in the World's Largest EV Market

Despite NIO's surprising struggles, the company can count on its home market, China to support its growth. China is the #1 EV market globally, retaking the lead it briefly lost to Europe in 2020.

BloombergNEF estimated that EV share of total China car sales will reach 25% in 2025, up from just 6% in 2020. China's government projections are slightly more conservative,putting it at 20% by 2025. However, China's EV sales outperformed these estimates as EV share of total sales reached 17.5% in September and averaged 13% YTD through September.

Hence, we believe the massive secular tailwinds underpinned by China's national agenda in EV adoption will continue driving growth for NIO.

Notably, the company expects China to be its most important market even as it charts its European (the world #2 EV market) expansion. NIO CEO William Li emphasized:

If we look at the global market, we can see that China is still the biggest auto market and the biggest premium market, so China will still be the most important market for us. But I believe for the markets outside of China in the long term, they should account for around 50% of the -- of all sales of our product. (from NIO's FQ3'21 earnings call)

Therefore, we expect China to continue driving the growth of the company moving forward as it scales. NIO highlighted that it currently has a maximum annual production capacity of 600K. Therefore, the company has positioned itself very well to scale its production moving forward. Considering its current YTD deliveries, we believe NIO's market opportunity is still in the early innings.

NIO's Fledgling Market Opportunity

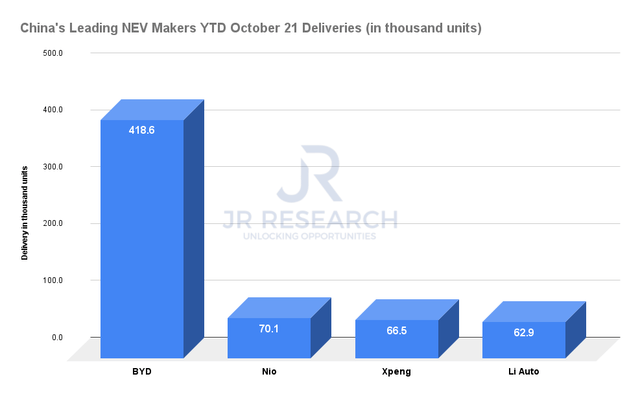

BYD Company Limited (OTCPK:BYDDF) is China's leading NEV maker. Its YTD deliveries (through October 21) highlight the company's undisputed leadership. We also discussed BYD's thesis in a recent article. Notwithstanding, NIO continues to lead its pure-play peers on YTD deliveries. However, the competition is very close. Nonetheless, we believe that China's massive tailwinds driving EV adoptions would continue to benefit NIO and its peers.

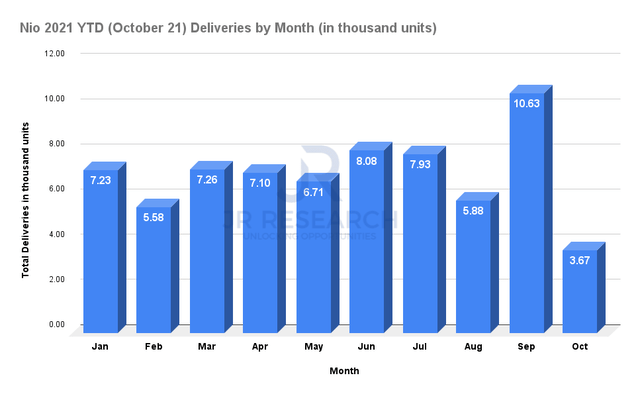

In addition, even though NIO reported underwhelming October delivery numbers, we don't believe it's a cause of concern. We will touch more on that later.

Readers can observe the "abnormally" weak October delivery numbers of 3.67K. However, we are not unduly concerned about October's numbers. The company telegraphed it needed some downtime to adjust its manufacturing processes to scale ET7 (NIO's upcoming flagship sedan). Notably, the company emphasized that it has "resumed normal production since late October." Li articulated (edited for brevity):

...To prepare for further capacity expansion and new product introductions including ET7, we implemented upgrades and the restructuring of the manufacturing lines at the Hefei JAC-NIO Advanced Manufacturing Center. Affected by the upgrades and the restructuring, we delivered 3,667 vehicles in October. The plant has resumed normal production since late October. (from NIO's FQ3'21 earnings call)

Therefore, we are not too concerned with October's problems. The company guided Q4 deliveries to be between 23.5K to 25.5K. Hence, Q4 deliveries are estimated to be about 24.5K at the midpoint of NIO's guidance. Therefore, QoQ growth is estimated to be flat. Notwithstanding, if we account for October's "abnormally" weak numbers, the company expects strong deliveries in November and December. On average, the company expects to deliver about 10.42K units each month for November and December, respectively. That would place it in line with September's record month of 10.63K deliveries. Therefore, the worries about October's weakness have been overblown.

NIO's expected deliveries for FY21 would amount to about 90.9K units. Compared to its annual production capacity of 600K units, it's clear that NIO expects to ramp production rapidly moving forward. While it might take some time to reach the 600K annualized run rate, NIO is preparing to launch 3 new products (including ET7) based on its NIO Technology Platform 2.0 in 2022. Therefore, the company is actively refreshing its slate and expects to continue its rapid delivery growth next year.

Notably, the company also expects to navigate the chip supply crunch well. It has also impacted NIO in the near term. However, NIO demonstrated its capabilities on its in-house technology as Li explained that they have managed to get around those problems. Li added:

I would like to specifically mention that because the many domain controllers in our vehicles are actually developed by ourselves in-house. So if there is a shortage of certain chips in the domain controllers, our teams have the capability to quickly find the alternative and do the rapid validation and faster production of those vehicles and the chips. So because of these capabilities, we have already resolved some chip shortage situations happened to our vehicles. (from NIO's FQ3 earnings call)

Consensus Estimates Also Agree With NIO's Rapid Expansion

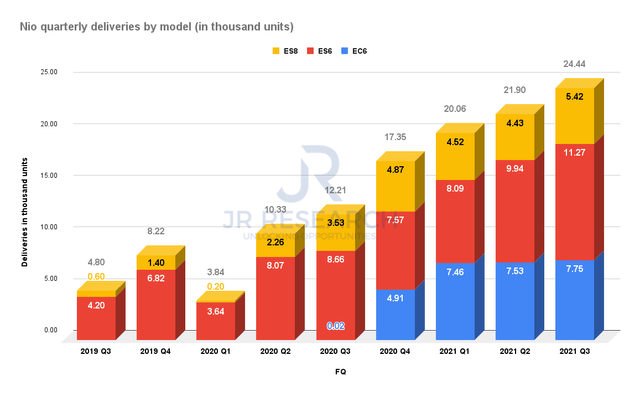

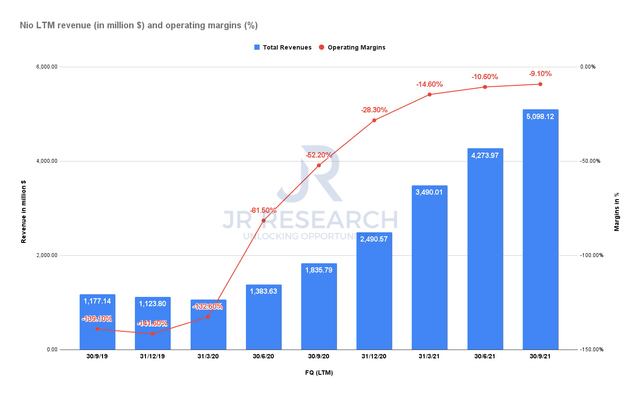

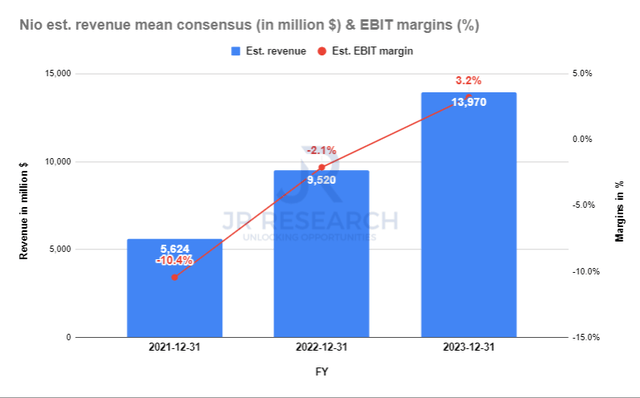

Readers can quickly glean from the first chart above that NIO has expanded its top line rapidly. Notably, it has also managed to improve its operating leverage tremendously as it scales. As explained, we believe that NIO is very early on in its profitability growth. Given that it has an annualized production capacity of 600K, NIO is still expected to grow rapidly. The company is estimated to grow its top line by a phenomenal CAGR of 77.7% through FY23.

Notably, its EBIT consensus estimates also point to a lower EBIT loss margin of 2.1% in FY22. NIO is estimated to turn EBIT profitable by FY23, with an est. EBIT margin of 3.2%.

Therefore, NIO investors can continue to expect the company to gain traction in its European journey and its home market. In addition, we encourage investors to pay close attention to its new product launches in 2022 as the company expects a strong delivery cadence moving forward. Notwithstanding, based on FQ4'21's guidance, November and December delivery numbers should also be impressive.

So, is NIO Stock a Buy Now?

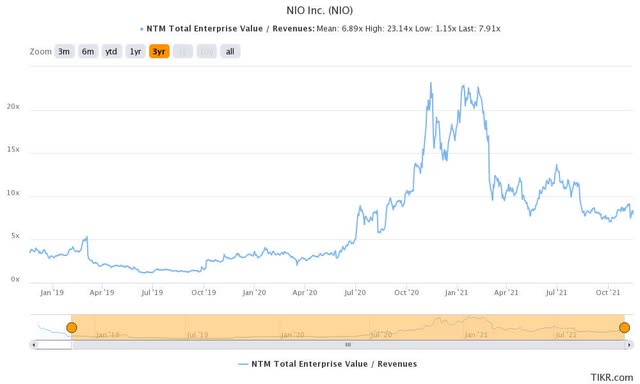

NIO stock is trading at an EV/NTM Revenue of 7.9x. It has come a long way down from its January highs. Moreover, it's also just about 14% above its 3Y mean. Therefore, we believe that NIO stock's valuation seems attractive now. It's a much stronger company than it was three years ago. In addition, it has also significantly improved its operating leverage. Coupled with strong secular drivers underpinning its rapid growth ahead, we believe long-term investors would do well to sit on it. If NIO can continue to build on its delivery cadence, we think that the stock will be re-rated moving ahead in FY22. Therefore, investors should capitalize on its weakness now to add NIO stock to their portfolios.

Consequently, werate NIO stock at Buy.