Summary

- AMD's margin gains are driven by growing strength in end markets.

- AMD raised its revenue guidance by $1.0B for FY 2021 and gross margins are edging closer to 50%.

- The semiconductor firm could be a $6.0B free cash flow business next year, even if growth slows down.

- AMD's dollar sales growth is cheaper than Nvidia's and AMD might even grow faster.

AMD (AMD) made a splash yesterday after the semiconductor company reported growth and margins that were even better than what was expected. AMD’s revenue acceleration and strong gross margin expansion make a strong case for upside in the stock.

Why AMD is worth $120

Before I dive into AMD’s latestresults, let’s quickly recap what the firm’s guidance was for the last quarter. For Q2’21, AMD expected a minimum of $3.5B in revenues with “high case” guidance implying 7% revenue growth Q/Q and a gross margin of 47%.

I expected AMD’s revenues to hit the high end of guidance ($3.7B), to have a minimum free cash flow of $895M (8% Q/Q growth) and a free cash flow margin of 24%. Given the acceleration of sales in higher-priced Ryzen desktop and notebook processors and GPUs as well as higher average selling prices/ASPs driven by broad-based strength in end markets, I expected AMD to beat its own margin guidance and report a gross margin of 48% for Q2’21. I also predicted a refreshment of AMD’s gross margin guidance due to strength in CPU and GPU ASPs. I laid out my forecast for AMD’s Q2’21 earnings in detail inAMD: On The Road To $5 Billion In Annual Free Cash Flow.

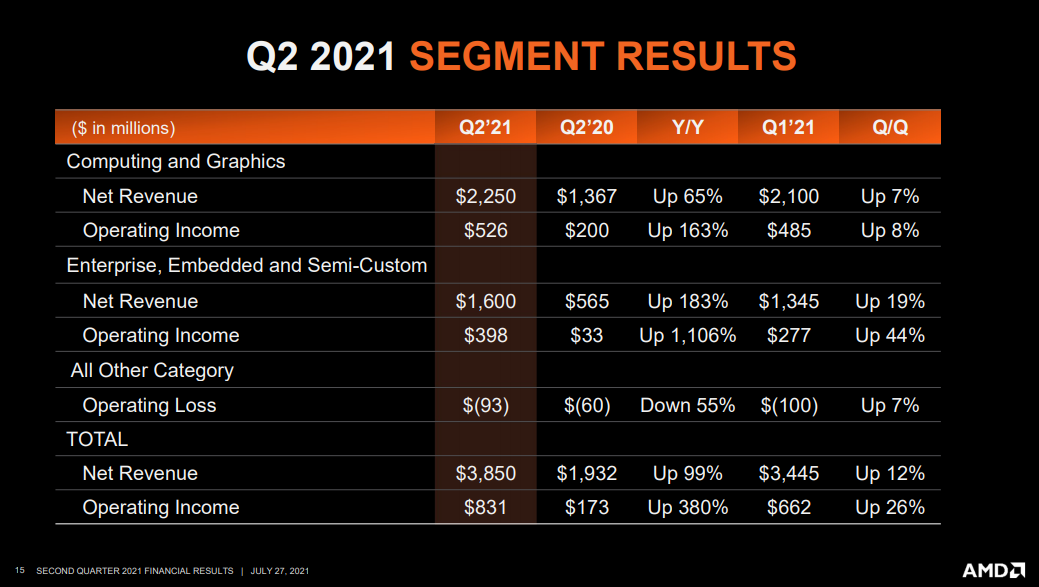

Turning to AMD’s actual results, the semiconductor firm proved once more that it is firing on all cylinders. AMD’s Q2’21 revenues were $3,850M, $150M above the high-end of guidance and up 12% Q/Q, with revenue momentum continuing in both Graphics/Computing and Enterprise markets. Graphics/Computing revenues increased 7% Q/Q to $2,250M because of higher client and graphic processor sales as well as strengthening ASPs. Enterprise, which has become the driver of AMD’s sales growth in recent quarters, saw Q2'21 revenues of $1.6B, up 19% Q/Q. Enterprise revenues continued to accelerate in Q2'21, after AMD recorded 5% Q/Q revenue growth in Q1'21.

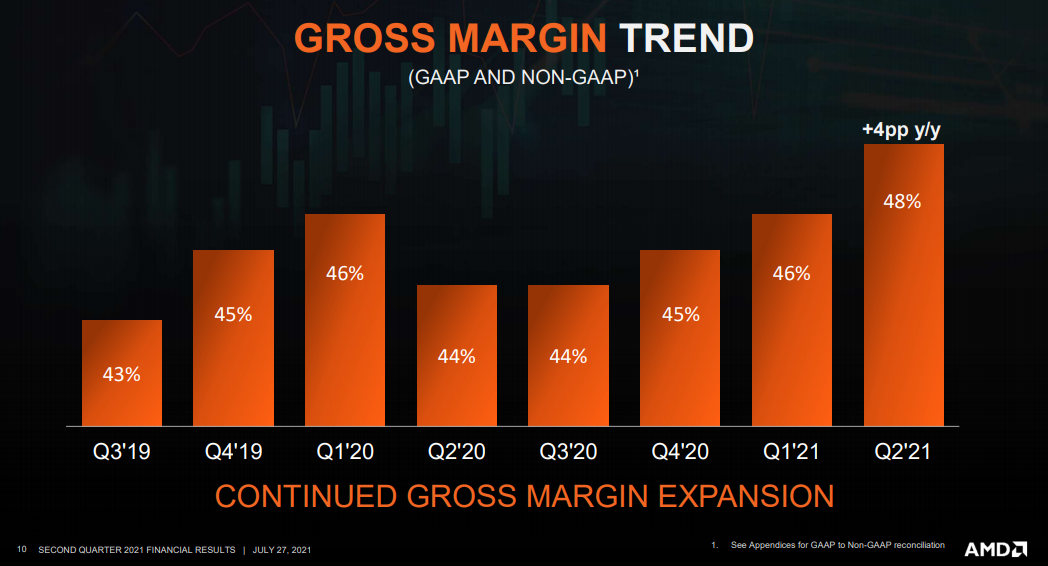

The most interesting revelation of AMD’s Q2’21 earnings, however, was the trend in gross margins. AMD's gross margin jumped 4 PP to 48%, 1 PP above guidance because of a better mix of higher-priced Ryzen processors (both mobile and desktop) and Radeon graphic cards. The uptick in gross margins in Q2’21 marked the third straight quarter of margin expansion for AMD and I don’t believe AMD has seen the end of this trend yet.

Turning to cash flow.

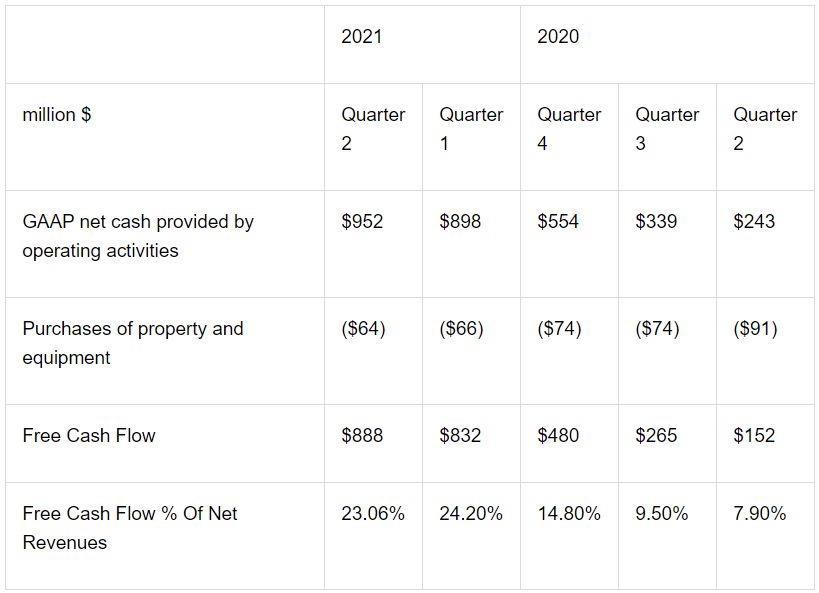

AMD reported cash flow from operating activities of $952M and free cash flow of $888M, $7M short of my expectation, but still almost six times more than a year ago. As AMD continues to see strong revenue growth tailwinds in both Computing/Graphics and Enterprise end markets, I believe AMD could grow its free cash flow margin to 30% by the end of next year. AMD raised its revenue guidance for FY 2021 (discussed later) by $1.0B which means I am also refreshing my free cash flow expectations for this year and next year.

AMD expects to have revenues of $15.6B this year. Assuming a stable free cash flow margin of 23-24%, AMD is looking at free cash flow of $3.6B to $3.7B. Revenue estimates for next year are not refreshed yet, but AMD should have revenues of at least $20B in FY 2022 (assuming 25% Y/Y growth), implying free cash flow of $4.6B to $4.8B next year… and these estimates do not account for the possibility that AMD’s 3rd-gen EPYC Milan-powered server processors and higher-priced GPUs improve AMD’s free cash flow margin. A 30% free cash flow margin next year implies a free cash flow of $6.0B.

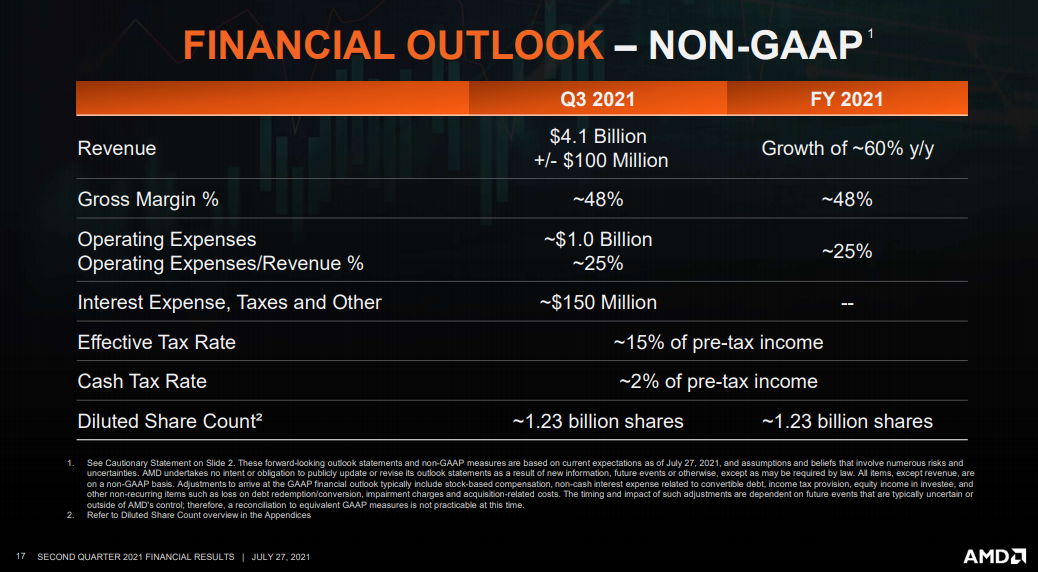

AMD is guiding for $4.1B in revenues +/- $100 million and the firm refreshed its FY 2021 revenue and gross margin guidance (as predicted). AMD now expects 60% revenue growth for FY 2021 (before 50%) and a gross margin of 48% (before 47%). Assuming 60% revenue growth, AMD is now looking at full year revenues of $15.6B (before $14.6B), so AMD's new guidance calls for $1.0B in additional revenues that were so far not priced into AMD’s market value.

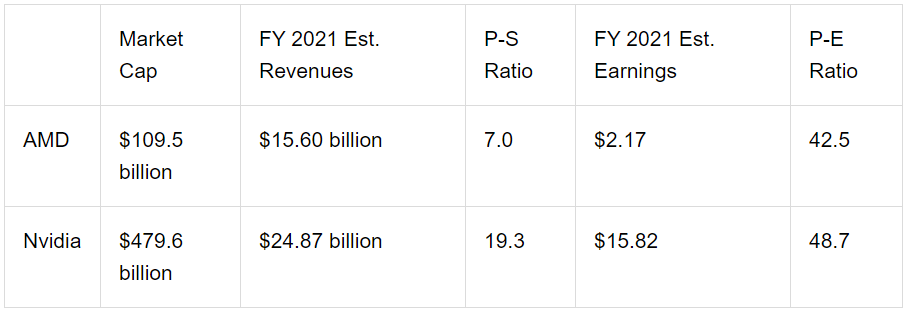

AMD’s higher gross margins and sales guidance create a potent force for the firm’s stock to revalue higher. Because of the recent dip in AMD’s shares and the addition of $1.0B in revenues, AMD’s dollar sales growth has become even cheaper after earnings. AMD’s dollar sales growth is valued lower than Nvidia’s and AMD is growing potentially at a faster rate: AMD's revenue guidance calls for 60% Y/Y growth and estimates for Nvidia imply "only" 49% Y/Y revenue growth for FY 2021. AMD has a market-capitalization-to-earnings ratio of 42.5 which is low for a firm that grows revenues 60% and that has a gross margin closing in on 50%.

Nvidia’s P-E ratio based on an FY 2022 EPS of $17.29 is 44.5. If AMD earnings growth (FY 2022 EPS of $2.71) was valued the same as Nvidia’s, AMD’s fair price would be $120 ($2.71 x 44.5 earnings multiplier factor), indicating 17% upside.

Challenges to my price target

The biggest opportunities and the biggest risks for AMD are tied to gross margins. AMD is having a year of strong revenue acceleration and margin growth, which is the chief reason why I believe AMD can revalue higher. But gross margins can't grow 3-4 PP every quarter. If AMD's gross margin expansion slows, or worse, gross margins drop back to 40%, decreasing stock returns for AMD are likely. A reversal in the gross margin trend would change my opinion on AMD and put my $120 stock price target in jeopardy.

Softening ASPs for CPUs and graphic chips are likely going to be the canary in the coal mine and could indicate weakening end markets for AMD ahead of time. Softer end markets imply AMD's revenue growth will slow which could result in a lower earnings multiplier factor by which AMD's profits are valued. I don't believe AMD is overvalued based on earnings, but the market may disagree with my assessment at any time.

Final thoughts

AMD reported impressive revenue growth and gross margins for Q2. AMD's raised guidance and Q/Q revenue acceleration indicate that end markets for CPUs and GPUs are a lot stronger than expected. This could lead to another year of revenue acceleration and a continual expansion of AMD’s gross margin to 50%, supported by rising ASPs. AMD's risk profile is still heavily skewed to the upside.