Summary

- Unity is the leading engine in real-time 3D for gaming creators. Moreover, its use cases have expanded beyond gaming.

- It recently closed its Weta Digital acquisition. We believe the deal is transformative.

- Its stock has also dropped 30% from its all-time high following its momentum spike.

- We discuss why we think investors can consider the opportunity to buy now.

Investment Thesis

Unity Software Inc. (U) stock suffered a well-deserved battering recently as sellers took control. The retracement knocked its price level back to more reasonable levels after dropping 30% from its all-time high. Impatient investors had driven the stock up as it reported robust earnings, coupled with the euphoria surrounding its Weta Digital acquisition. The bull-trap was well-laid by the market makers, and these investors have been given invaluable lessons about patience and valuation.

Nevertheless, we have been bullish on Unity stock throughout the year. Our bullish calls in May and June are still up 62% and 32%, respectively. However, we updated in a recent November article cautioning investors not to chase the hype and revised our rating to Neutral. The stock has fallen 20% since the article was published.

Moreover, thanks to the steep retracement in growth stocks recently, we believe that the time has come for us to revisit our rating. We discuss why we think investors who have been biding their time can consider adding exposure.

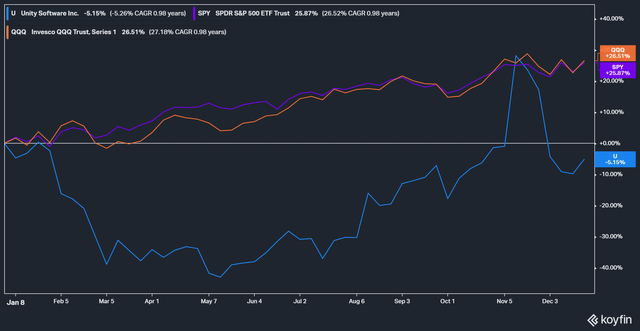

U Stock YTD Performance

Unity stock has had a disappointing year until its upward momentum started to recover in H2'21. We also saw the opportunity from its mispricing in May and June and thus encouraged investors to accumulate. The stock was on a steady climb towards its recovery until the momentum spike catapulted its YTD gain to 28% in November. However, the euphoria was short-lived as Unity stock's valuation returned to haunt investors who joined the "spike bandwagon." After its recent retracement, the stock is back in the red for the year, with a YTD return of -5.2%, significantly underperforming the market.

Why We are Turning Bullish On Unity Stock?

We took the opportunity to pare down our exposure in the recent spike and rotated to other undervalued growth stocks. However, we always intend to add exposure again when the euphoria has dissipated. Unity's robust FQ3 report card demonstrated that the company is still barely scratching the surface of its massive TAM, which expanded to $45B recently. The company has also completed its acquisition of Weta Digital on 1 December, as it works on integrating Weta Digital's unique technology stack into its offerings. The deal also brought 275 world-class engineers into Unity's payroll, which the company believes is some of the best talents that Weta Digital has recruited. Unity emphasized (edited): "These 275 people, they're extraordinary. They're PhDs, research scientists. They've been focused on graphics research for 20 years. If you go to SIGGRAPH and look through papers… it just goes Weta, Weta, Weta."

Therefore, we firmly believe that it's a transformative acquisition for Unity. Creators have already used the company's solutions across multiple industries, most notably in gaming. In addition, the company has documented numerous industrial and commercial use cases as enterprise customers realize the power of its real-time 3D engine.

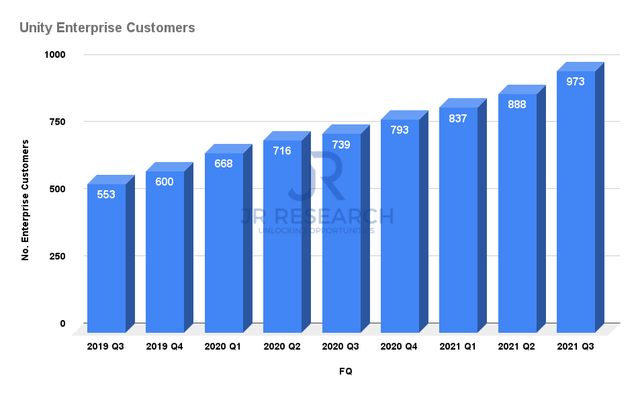

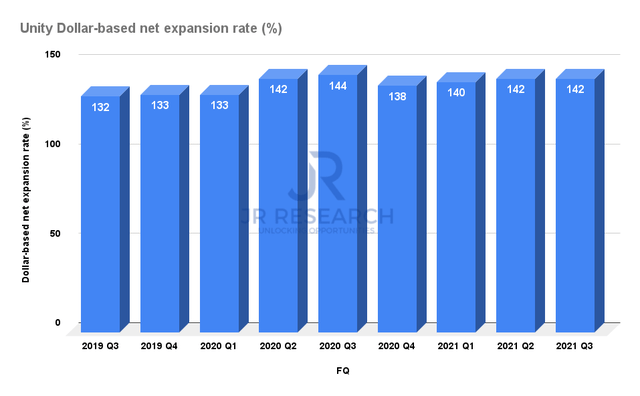

Consequently, Unity continues to experience stellar growth in its enterprise base. Its enterprise customer grew from just 553 in FQ3'19 to 973 in FQ3'21, representing a CAGR of 32.7%. Moreover, its customers continue to expand their use cases consistently. As a result, its net expansion rate has maintained around 140% over time. Therefore, the company has sustained robust monetization in its Operate solutions while driving new use cases through its Create solutions.

While it's still early to determine the expansion of new or expanded use cases linked to Weta's technology stack, Unity is confident that it can leverage strongly. In addition, it has an eye on the multi-trillion-dollar metaverse, as it aims to be one of the critical engines for creators. Unity General Manager Marc Whitten emphasized (edited):

The key for me - I strongly believe, whatever word you want to use for the metaverse, it's going to need more 3D content. It's going to need an extraordinary increase in the number of people capable of building in 3D. Certainly from a Unity perspective, we really started thinking hard about how we could build something that democratizes content creation. Between Unity and Weta, we had the tools to do something extraordinary. You have this set of people at Weta who had built the most spectacular tools ever for 3D content creation that had never been productized. And then you have Unity, where our bread and butter is packaging and democratizing tools and making them more accessible. It became more and more clear that we could find the right transaction to make it happen. (VentureBeat)

It's also essential for readers to note Weta's highly scalable tools. Unity articulated that Weta has an "incredibly forward-looking architectural approach." They use "one data model, one data river, and a set of tools that impact that. [It allows] individuals to see how things show up across multiple objects, or multiple artists to be able to collaborate and work in parallel and do amazing things around that." As a result, the company believes it can scale Weta's stack with its technology and extend the use cases well beyond gaming. CEO John Riccitiello added (edited):

I would expect the use cases to continue to grow. We see huge opportunities for us in media and entertainment, in games, adding more seats -- with artists. We believe there is an opportunity in architecture. We believe there are opportunities in automotive. So many, many different industries will continue to see growth. (Unity's FQ3'21 earnings call)

We have always believed that Unity's engine is the world leader in real-time 3D. Moreover, it has proven its use cases well beyond gaming. Furthermore, the Weta deal demonstrates how management intends to further consolidate its leadership against its peers by taking its competitive moat a step further. We love companies that are relentless in their pursuit of innovation.

Key Risks That Investors Should Consider?

The transformative acquisition is not cheap. But it shouldn't be cheap for a tech stack of this scale. The company closed the deal with a mix of cash and stock that amounted to $1.625B. Moreover, the company recently announced $1.5B in convertible senior notes, which would partly be used to fund its acquisitions. Given that the company had minimal long-term debt ($124M in FQ3) compared to cash and short-term investments of $1.28B, the size of the debt offering is massive. Therefore, Weta's acquisition has introduced significant execution and balance sheet risks that Unity needs to manage well.

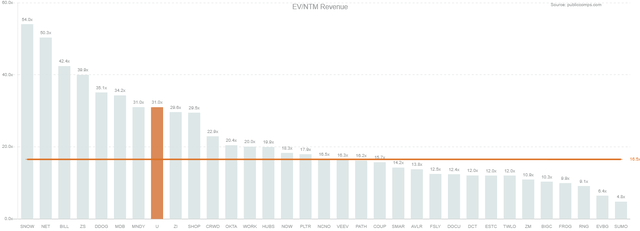

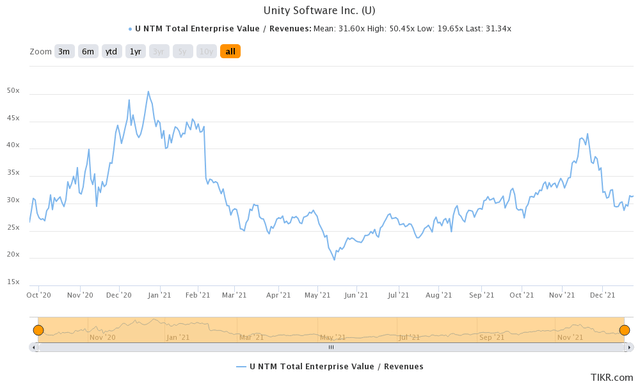

In addition, Unity stock is still priced at a significant premium. It is trading at an EV/NTM Revenue of 31.3x, well ahead of the high-growth SaaS comps median of 16.5x. Therefore, it's imperative for management to execute very well moving forward. Otherwise, the risks for significant value compressions could potentially occur.

Unity stock is highly volatile. Therefore, we have added the stock in batches throughout the year as we believe its inherent volatility should continue to create attractive opportunities. Hence, we have not joined impatient investors adding through the momentum spikes.

Nevertheless, Unity stock is trading near its 1Y revenue multiple mean. Despite that, it's clear that the stock is trading at a premium valuation.

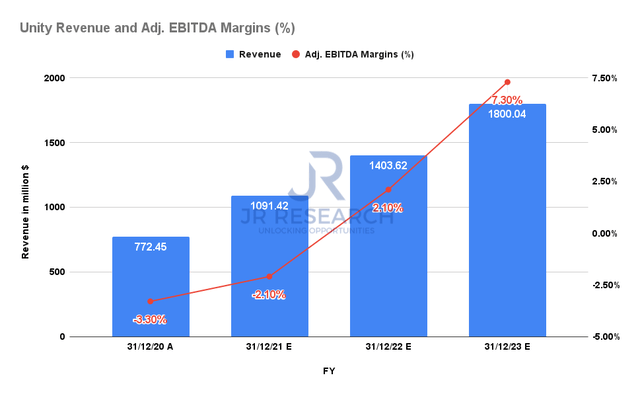

However, investors should note that Unity is estimated to gain significant operating leverage moving forward. Its top line is expected to increase at a CAGR of about 33% over the next three years (FY20-23). However, its adjusted EBITDA margin is projected to reach 7.3% in FY23, from -3.3% in the last FY. Hence, investors should start to pay more attention to Unity's bottom line growth moving forward. The company could begin gaining tremendous leverage and turn profitable on an adjusted EBITDA basis.

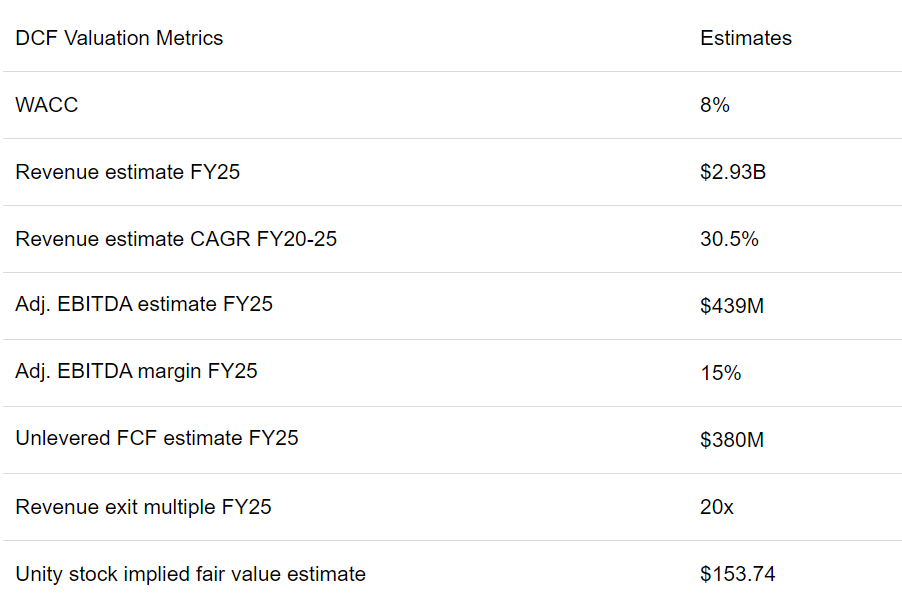

Consequently, we believe it's appropriate for us to apply a DCF valuation framework that accounts for its operating leverage moving forward. It would allow us to appreciate the impact of its profit drivers better.

Hence, Unity stock seems to be right in our fair value zone right now. Investors who need a more considerable margin of safety can continue to wait for a potentially deeper retracement. However, investors who have high conviction could use this opportunity to add exposure to a fantastic company.

Consequently,we revise our rating on Unity stock to Buy.