Summary

- Down over the past year, shares of Alibaba have not participated with the general rally in the markets.

- Alibaba is a strong business with accelerating free cash flow generation and a clean balance sheet. The company has deep pockets to continue growing.

- The valuation that shares trade at is compressed, but seems poised to rebound. Fundamentals eventually steer the share price.

E-commerce has been a powerful investing theme throughout the pandemic. While many stocks that sell over the internet have been thriving, Chinese conglomerate Alibaba Group Holding Limited (BABA) has been a notable laggard. Shares of Alibaba are in the red over the past year, while the S&P 500 has ripped higher, gaining 32%.

Alibaba has been caught in some controversy surrounding thefailed IPOof Ant Group and its founderJack Ma. While the market has focused on these distractions, the actual underlying business of Alibaba is performing at a high level. With strong fundamentals and rapidly growing free cash flow, it's only a matter of time before the market begins to focus on what matters...the business. We will outline our investment thesis below.

Free Cash Flow Growth Is Stellar

Alibaba is a frequently covered business on Seeking Alpha, so I won't rehash the basics about the business or dive into the political controversy that has plagued the stock. Instead, I want to focus on the financial inflection point that Alibaba has recently hit.

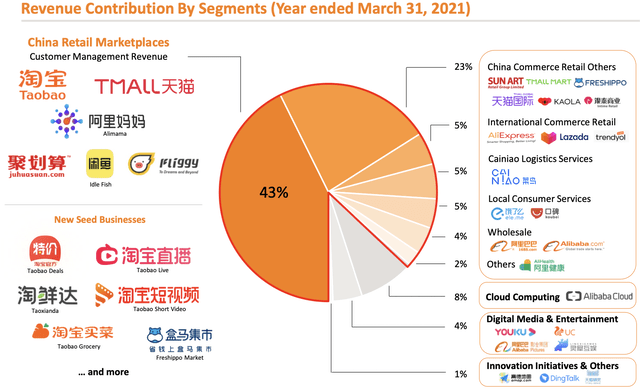

The company ended its fiscal year at the end of March. What we see is a diversified business with several growing segments that align with macroeconomic trends.

The largest revenue contributor, of course, is the company's retail operations. While its commerce segment continues to narrate revenue growth (total core commerce grew 2020 revenues 42% versus company revenues growing 41%), some smaller segments are showing strong growth.

For example, Alibaba's cloud computing operations grew 50% in 2020, and its new retail and direct sales businesses grew 94% year-over-year. What is most promising is that Alibaba is accelerating its free cash flow growth in recent years. The company's $26.35 billion in 2021 FCF is a 29% year-over-year jump from 2020. Alibaba grew FCF 25% from 2019 to 2020.

With $72 billion in cash on hand as of March 31st and the business generating more than $26 billion in free cash flow, Alibaba has deep pockets to develop its growing business segments and seek out opportunities to create new growth with M&A or other developments.

How Long Can Alibaba Stay "Cheap"?

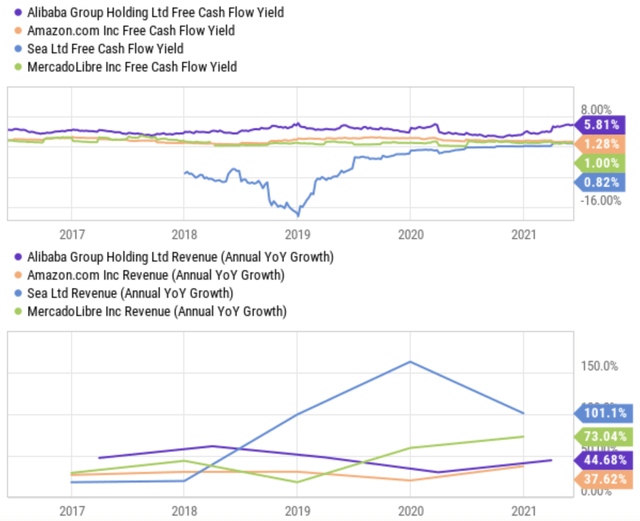

It's hard to understand just how beaten down Alibaba's stock is until you look at things from a free cash flow perspective. Alibaba is currently trading with an FCF yield approaching 6%. By comparison, the next highest FCF yield is Amazon (AMZN), with a yield of just 1.3%.

This is a tremendous discount to Alibaba's peer group, despite the company accelerating FCF growth and having a ton of cash on hand. And because Alibaba is a healthy and growing company, the stock is poised to become even more attractively valued.

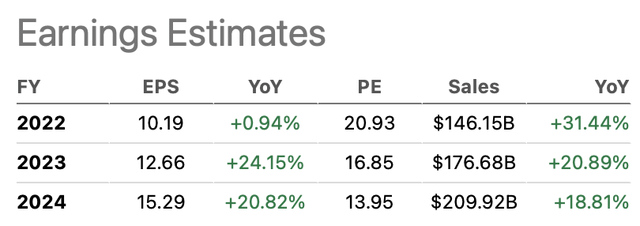

The company is estimated to continue growing revenues at a swift clip, approaching $210 billion in annual revenue over the next three years. If we apply the company's 24% conversion rate of revenue to FCF, that will give us 2024 FCF of $50 billion. In other words, an FCF yield of 8.6% on today's share price. This is simply something you don't often see for a company's stock growing so rapidly at such an already large size.

The stock is clearly being punished for some of the drama that Alibaba has faced over the past year and some of the current tension between the United States and China. This is a risk that investors need to keep in mind, as anything can happen, and Alibaba may become collateral damage of political conflict. However, if it becomes clear to the market that the outlook is promising, Alibaba could aggressively rerate. Even if Alibaba saw its FCF yield fall to around 3%, it would imply an upside in shares of 46%. This would put Alibaba at an enterprise value of more than $800 billion, but I believe those shoes the company could certainly fill.

Wrapping Up

Alibaba is a fantastic business that has been caught up in some political drama. Despite its size, the company is growing rapidly, is profitable, and generates tons of free cash flow. Investors cannot ignore the political risks, but the upside is tremendous for brave and patient investors.