Summary

- Another great quarter shows a high price may be justified.

- Growth in the Services business is more valuable than products.

- Apple looks like a great company, but a fairly valued one.

- No need to buy here, but no reason to sell either.

After another great quarter, I'm kind of awed by what Apple (AAPL) has accomplished, the number of customers who love their products and the financial results all that brings together. I'm genuinely surprised by how big these earnings numbers get. My goal here is just to explain how I would put a range of valuations on Apple's stock, and then we can work backwards to figure out what kinds of assumptions are "baked in" to different stock price levels.

Is this the best business in the world?

No less an authority than Warren Buffett has called Apple "probably the best business in the world" and it's easy to understand why. Apple's primary products are the iPhone (with popularaccessories) and Mac computers and the iPad.

For years I made the mistake of analyzing Apple's products by comparing their capabilities and specifications to other products at similar price points. This was a huge mistake. Rather, the right way to look at it in this case is how people feel about the company.Its products not only make people happy, but they have become part of people's identities. I wouldn't normally fawn over a company or its products in this way in an analytical article, but it's important for the next point I want to make.

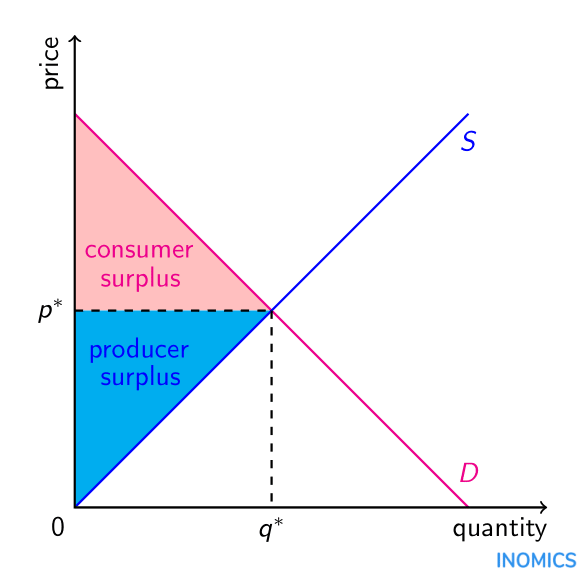

Because Apple's products are so highly valued by its customers, its products have a high consumer surplus (pink area in the graph below):

That is to say that many people would be willing to pay more for what they get from their iPhones. This means two important things for Apple's business. First, they have some room to increase prices over time. Second, it would be very difficult for a competitor to offer something else as satisfying at a similar price. That means that Apple pursues a profit-maximizing strategy by keeping its prices relatively low compared to what it could charge(i.e., how many people do you know who already have iPhones would pick a different phone even if they had to pay an extra $100?).

And still, the earnings power of the business is enormous.

Third Quarter earnings look great

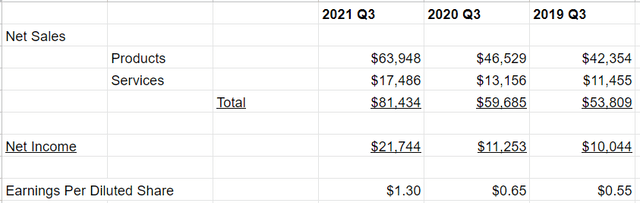

Apple's third quarter resultswere extremely strong, with almost $82 billion in sales and over $21 billion in net income. News reports have talked about year-over-year growth and I assumed that Apple would be merely overcoming an "easy comp" since one year ago was some of the worst of the Covid-19 pandemic and lockdowns. That is to say I expected this quarter to be weak in its own right and subsequent results would not only be coming off an unusually low base, but would also include some delayed purchases as people who would have bought early "caught up."

Instead I was surprised to find that Apple also grew in the third quarter of 2020 (Apple's fiscal year ends at the end of September, so we're in the third quarter)! This spreadsheet shows how revenue and earnings have grown in the last threeyears' worth of third quarters:

So as we can see, Apple in fact grew earnings through both product sales and services in the depths of the pandemic. So if there's an "easy comp" problem, it's still in a business that grew anyhow. Just as likely is that without the option to travel or eat in restaurants, people with disposable income were more likely to spend on Apple products.

This was just a great quarter.

A simple model for Apple's earnings

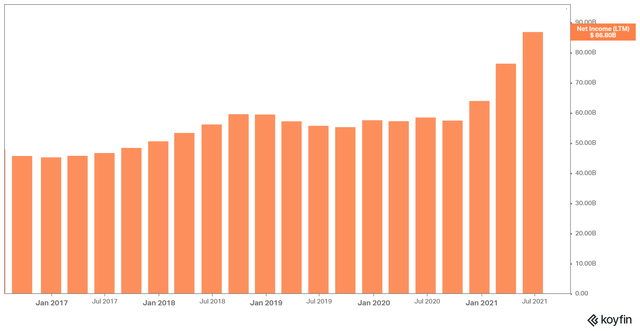

The job now is to put this in context. I made this chart using Apple's trailing twelve month earnings for the last five years to show not only the scale but also the growth of what we're talking about:

For the last four quarters, net income is $86 billion. But as we saw above, Apple breaks its sales into two segments, products and services. And services is growing apace.

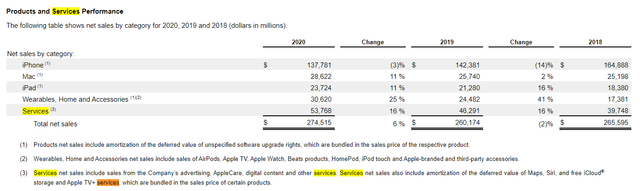

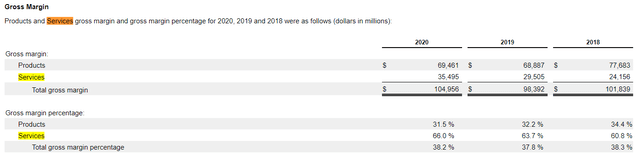

These two items from Apple's last annual report tell the tale of a growing and increasingly profitable services business:

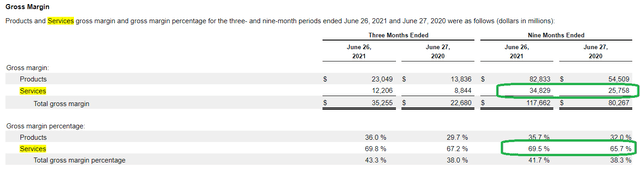

As you can see in the first chart, Services revenue grew over three years from almost $40 billion to almost $54 billion, and in the second chart you can see that it became increasingly profitable with gross margins increasing as revenue increased. This is common in software and media endeavors; if your service can pay the bills with 1 million customers and you add another customer for free, each additional one is "pure profit." We can see that these trends have only increased in the first three quarters of this year:

So all this is to say that rather than use the $86 billion number to value Apple going forward, I want to put separate multiples on the "Products" and "Services" businesses.

For the last nine months, Apple had a gross margin of almost $118 billion. In the same 10Q they reported $32.5 billion in operating expenses and $11.8 billion in income taxes. If we considered these Products and Services assumptions as separate businesses and allocated those expenses and taxes among them, I would do it in proportion to their share of gross margin. So 29% of that $32.5 billion in operating expenses and $11.8 billion in income taxes goes to Services, and 71% to Products.

For the last nine months, that means Products would have earned $51 billion and Services would have earned $25 billion. I realize this rough number is 2 billion higher than the amount Apple reported as net income, but that's OK since we're making a lot of assumptions here.

In last year's fourth quarter Apple only earned slightly more than in the third. So to estimate a full year, I'm just multiplying my nine-month numbers by 4/3. I get a full year estimates of the following by segment:

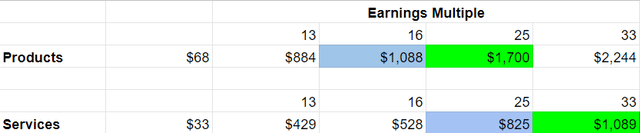

Products: $68 billion

Services: $33 billion

To arrive at a valuation, I want to offer a range of multiples and let the reader find the number that seems most reasonable to her:

So using my "back-of-the-envelope" numbers, I would feel pretty comfortable buying Apple at a 16x multiple for its products business and a 25x multiple for its services, which yields and an enterprise value of $1,088 + $825 = $1,913. Throw in Apple's $89 billion in additional net cash, and I would be interested in buying shares at a market capitalization of $2,002 billion, or about 16% below recent prices - namely $123 per share.

On the other hand, I would start to be concerned that if we paid more than 25x for the Products business and 33x for the services business that perhaps the valuation is getting ahead of itself. So at a market cap of $1,700 + $1089 + $89 = $2,878 billion or $173 share, I would think that's too high a price to pay today to earn a good return.

Conclusion

There are a lot of things that could go keep Apple from being a good investment, but it's hard to imagine them when looking at results like this. I wouldn't be concerned about someone else building a better phone. Rather what would concern me most are the "unknown unknowns" such as some kid of change of technology that makes Apple's advantage in customer satisfaction from the iPhone not that relevant.

I wish I could reach more of a firm buy/sell conclusion about Apple's share price here, but it looks fairly valued to me based on some reasonable assumptions. I would be interested in buying (or selling puts) below $120 share.