Summary

- Shopify has consistently delivered for long-term investors who have kept faith with the company despite its high valuations.

- The company has multiple growth drivers in Payments, and International markets to further drive its growth story.

- Its technical picture also shows a stock that has always been strongly supported along its long-term uptrend.

- I attempt to discuss the key aspects of its operating performances and why investors should also focus on international expansion as a key aspect of e-commerce growth.

Shopify (SHOP) is one of the most hotly debated e-commerce stocks because of its explosive revenue growth rates and its high valuations. The company continues to demonstrate both stellar topline and bottomline growth while also improving its cash flow margins. The management’s ability to monetize its merchants through Shopify Payments and its suite of merchant solutions is a masterstroke that shows the capability of the management to be able to continue executing its high growth strategies with aplomb moving forward. Despite its relatively high valuation levels, it also remains a very strong stock from the technical point of view, so bullish investors may consider adding it at the next dip.

Shopify: Defying Amazon’s Valuation Logic

Shopify’s critics have often questioned the logic of investing in Shopify when you can invest in Amazon (AMZN) for a fraction of its expensive valuation. Yet, investors in SHOP continue to defy “common valuation logic” by pointing to Shopify’s incredible growth rates.

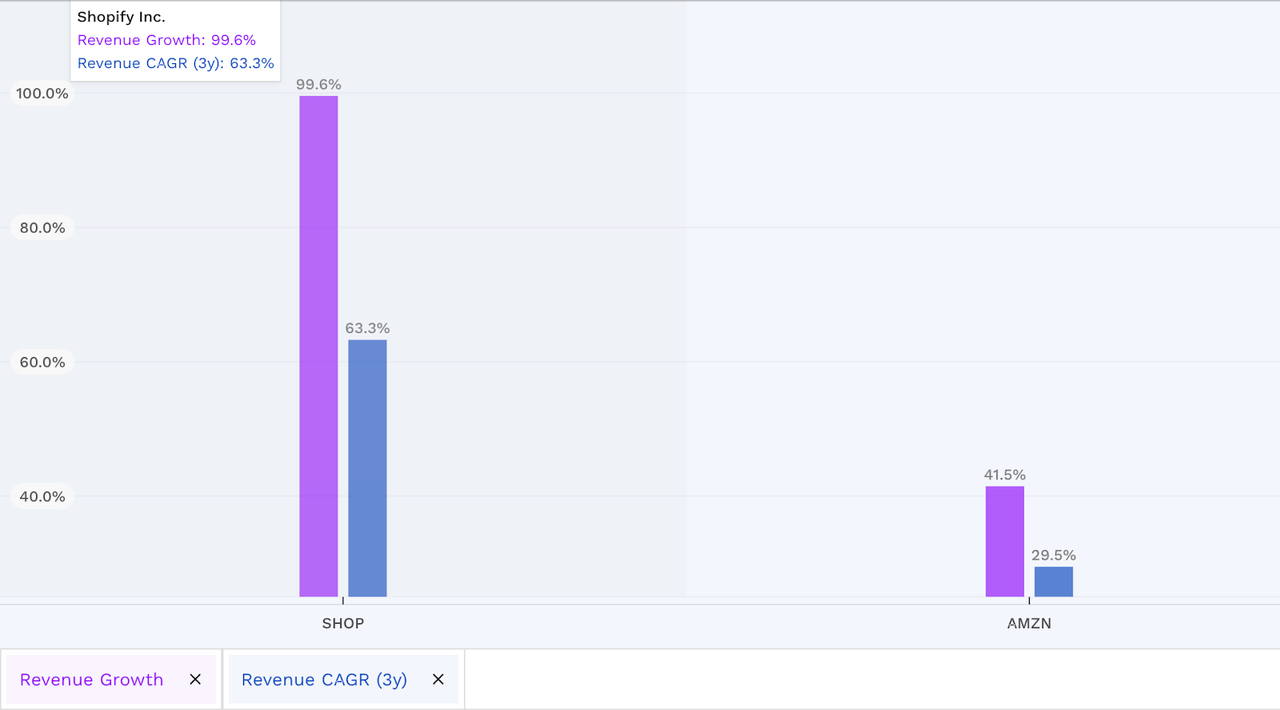

Over the last 5 years, SHOP’s revenue growth has easily surpassed AMZN at every reporting quarter, and the pandemic fueled e-commerce tailwind also drove higher growth to SHOP as its LTM revenue YoY growth read 99.6% as compared to AMZN’s “meagre” 41.5%. Moreover, SHOP’s revenue 3Y CAGR of 63.3% also easily bested AMZN’s 3Y CAGR of 29.5%. So clearly, SHOP’s growth has been truly phenomenal.

Shopify's Compelling Merchant Solutions Growth Drivers

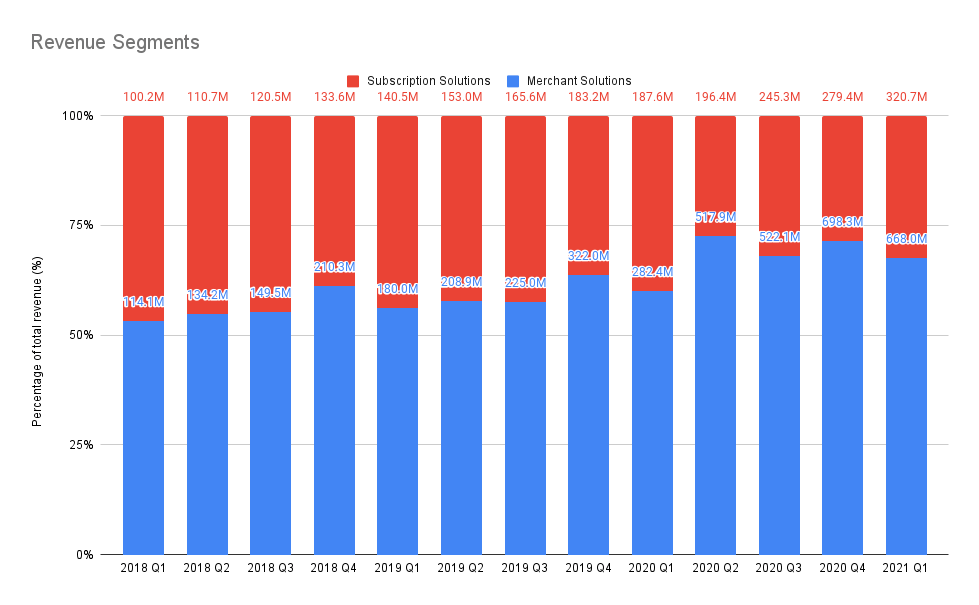

In recent years, we could see that even though Shopify’s revenue growth has been pretty much broad-based, its merchant solutions segment has been taking up an increasingly large contribution in the company’s revenue base and have transformed itself into Shopify’s most important revenue driver, accounting for 67.6% of Q1’21 revenue. The shift towards increasing the revenue base of merchant solutions has seen the company continuing to roll out multiple new merchant solutions initiatives and services to further monetize the company’s merchant base and improve the strength of its ecosystem, therefore enhancing its “stickiness” and retention over time.

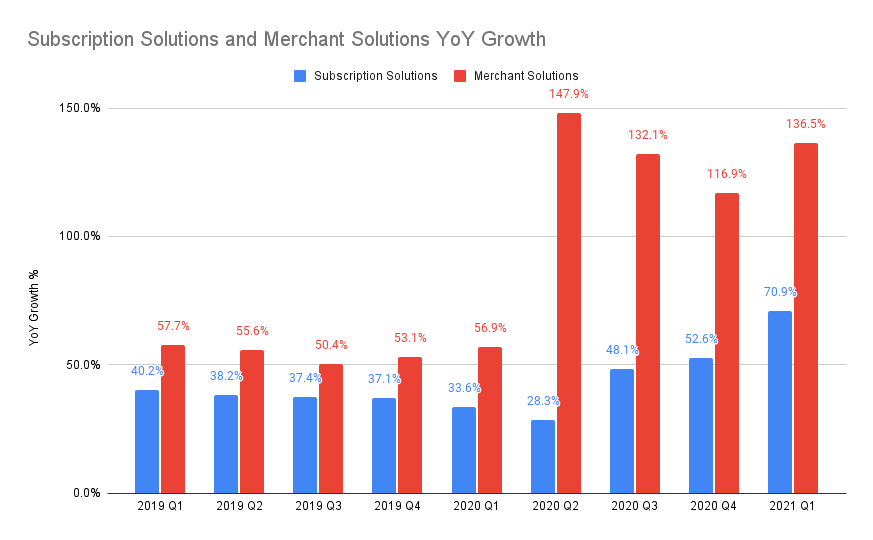

Investors should be careful not to get too excited with the pulled forward growth as a result of the COVID-19 pandemic that we observed in FY 20 as seen above. The management has already strongly emphasized in their guidance that they do not expect this to repeat, and expects YoY growth to normalize to levels seen before the pandemic, which in this case is estimated to be somewhere north of 50%. Even though growth is expected to normalize moving forward, it’s not as if SHOP has been growing slowly and more importantly the pulled forward growth last year has allowed SHOP to dramatically increase its merchants growth onto its platform for future monetization within Shopify’s robust ecosystem.

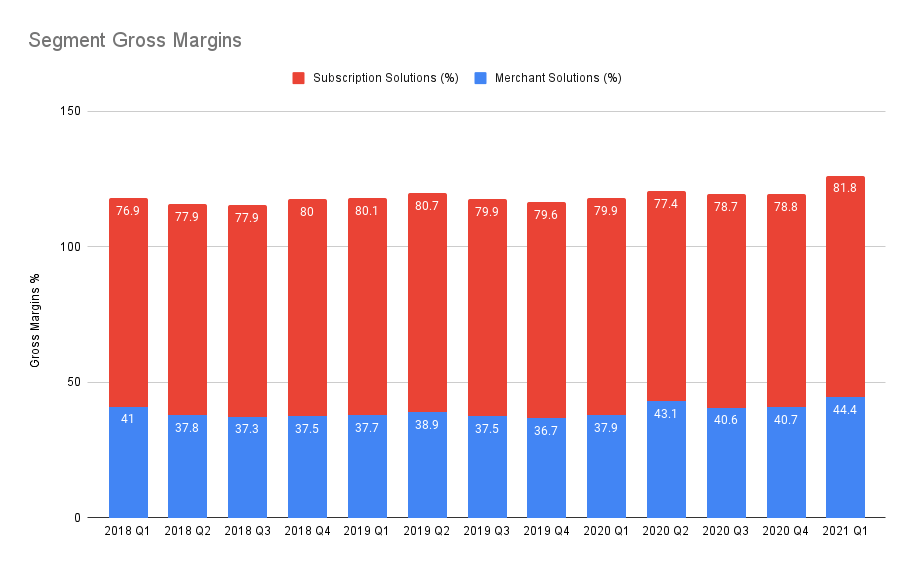

Although Q1’21’s gross margin was higher than recent historical trends, we should not expect this to carry on moving forward. The management pointed out clearly that the company is focusing its efforts to continue improving its robust ecosystem for its merchants such as developing the Shopify Fulfillment Network [SFN], as it expects that the merchant solutions segment to continue driving its revenue growth even if it means lesser gross margins moving forward.

Shopify Payments is the Key to Unlock the Benefits from GMV Growth

Despite that, the company clarified that as Shopify Payments continue to see increased adoption and usage among its merchants, the company expects to see significant improvement to its SG&A efficiencies as Shopify Payments has a much lesser impact on SG&A margins, therefore leading to improvement on operating efficiencies as Shopify Payments scale up further.

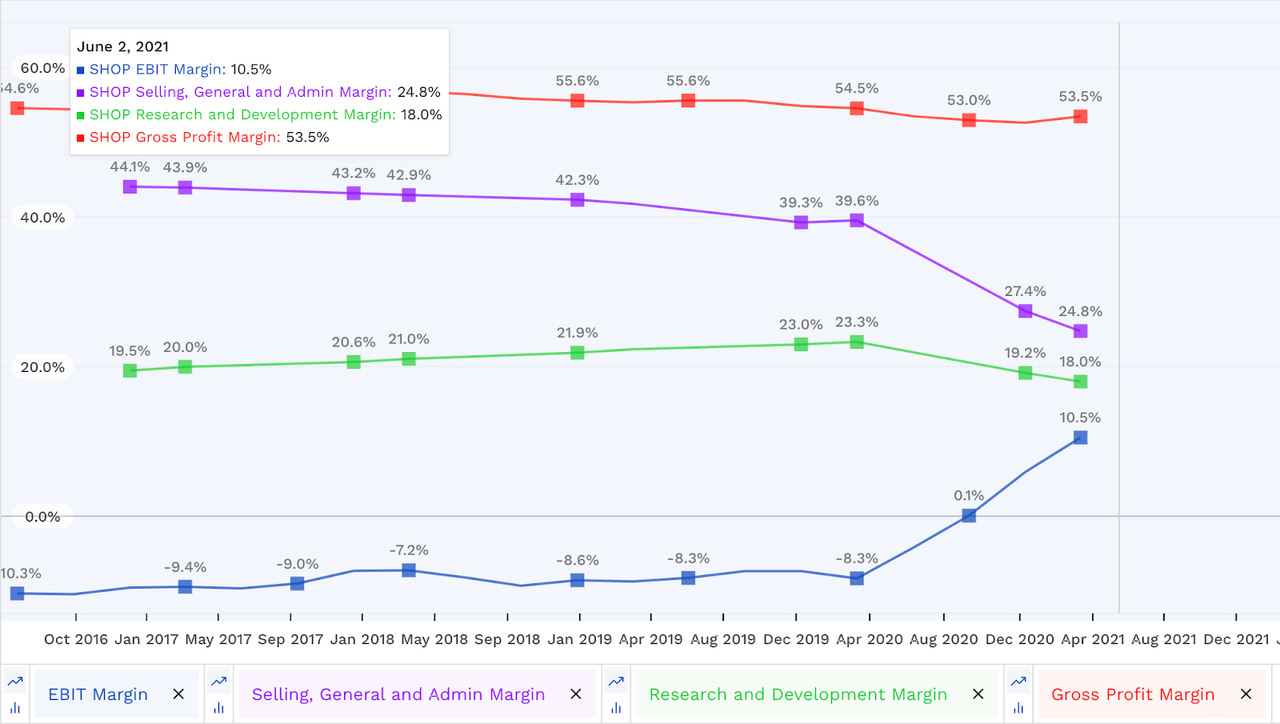

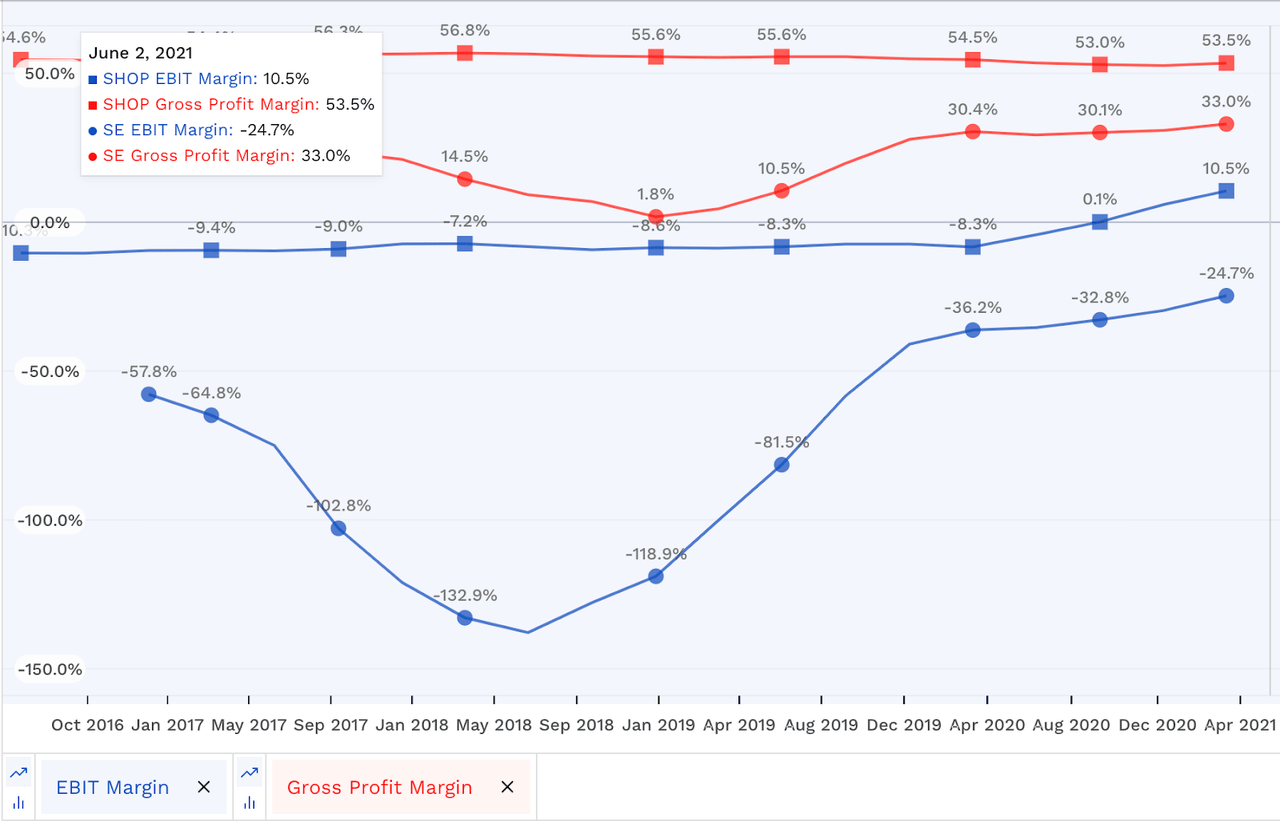

Clearly, investors could see that despite posting a relatively high LTM gross margin profile in Q1’21: 53.5%, it has only recently turned LTM EBIT profitable (Q1’21: 10.5%), thanks to the company’s solid improvement with its operating efficiencies even though the gross margin profile has remained stable over time, even with the pulled forward growth from COVID-19 last year.

We could see a consistently declining LTM SG&A margin trend reaching 24.8% in Q1’21 from a high of 44.1% in Q4’16, signifying a huge improvement. Therefore, I’m confident that SHOP would continue to deliver improved operating efficiencies as it scales up its SFN to further strengthen its ecosystem, creating even more value and synergies for its merchants and their customers.

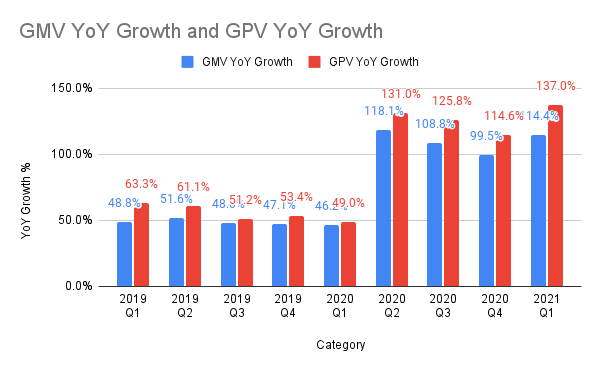

SHOP’s GMV and GPV Analysis. Data Source: Company Filings

We could clearly see the increasingly important role of Shopify Payments for its merchants as more and more merchants are using Shopify Payments over time as GPV growth has outpaced GMV growth consistently, with Q1’21 reading coming in at 137% YoY growth and 114.4% YoY growth, respectively.

With the increased adoption and usage of Shopify Payments, in Q1’21 GPV formed 46.4% of GMV, from a low of 37.5% of GMV just 3 years ago. I believe Shopify is moving in the right direction to continue driving more and more merchants towards Shopify Payments as it creates a powerful flywheel to unlock even more and more of the expected massive GMV growth moving forward.

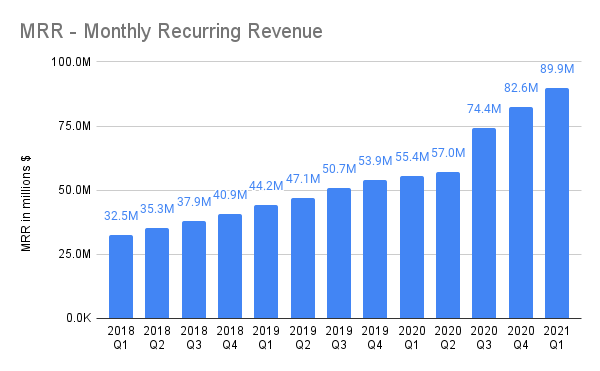

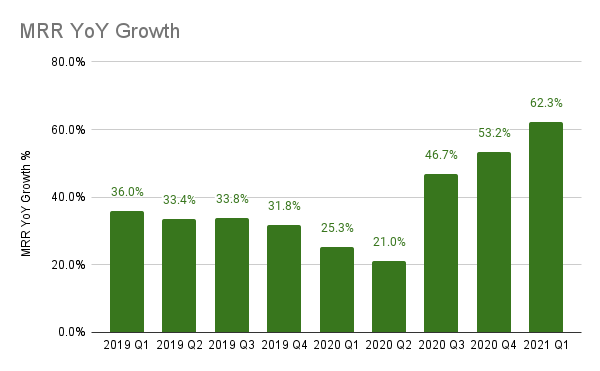

The sustained improvement in GPV growth has come at an important juncture as SHOP had already been experiencing slower MRR growth pre-pandemic (from 36% in Q1’19 to 21% in Q2’20). Therefore, by strategically being able to monetize its merchants in other areas has helped to manage this slowdown, while at the same time opened up many new revenue opportunities for Merchant Solutions to help drive the company’s future growth.

The Importance of International Expansion

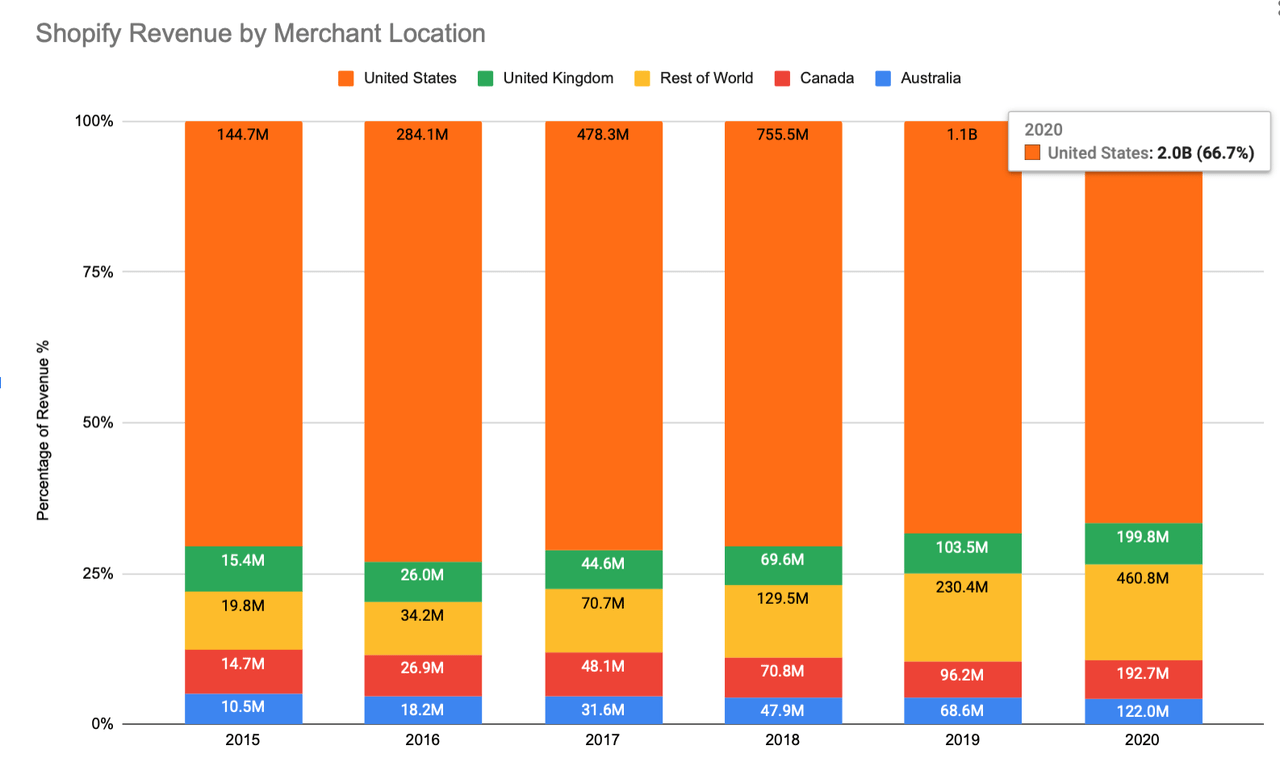

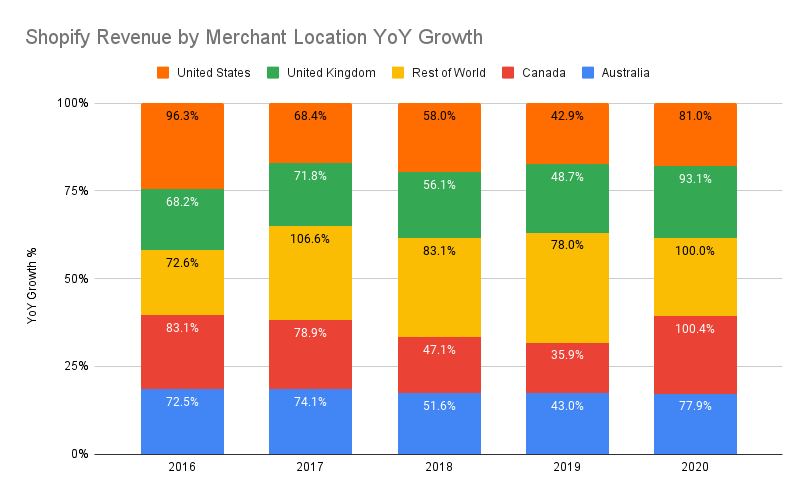

Although U.S. merchants continue to be SHOP’s most important revenue driver (66.7% of FY 20 revenue), the company has also experienced rapid growth in other geographical markets, particularly in its Rest of World segment. As we can observe from the above chart, U.S. growth has already been trending down pre-pandemic, while Rest of World growth has continued to grow rapidly and consistently.

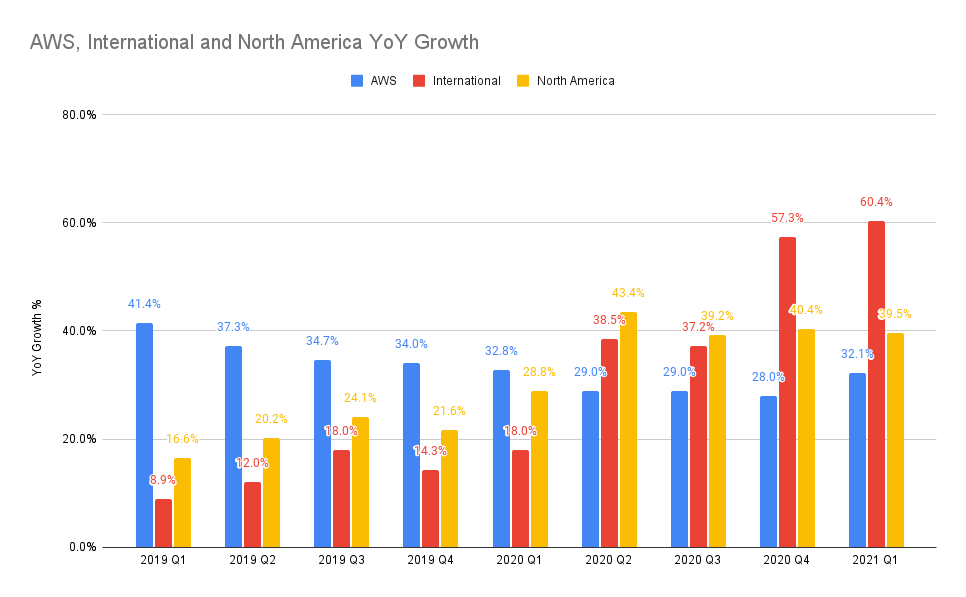

We also observed this from AMZN’s International segment growth where although it has been somewhat of a laggard in previous quarters, it has started to outpace North America’s growth for the last 2 quarters, culminating in Q1’21 YoY growth of 60.4% for the International segment against 39.5% for the North America segment.

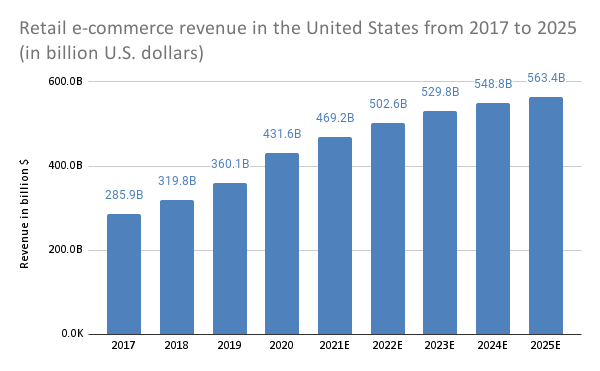

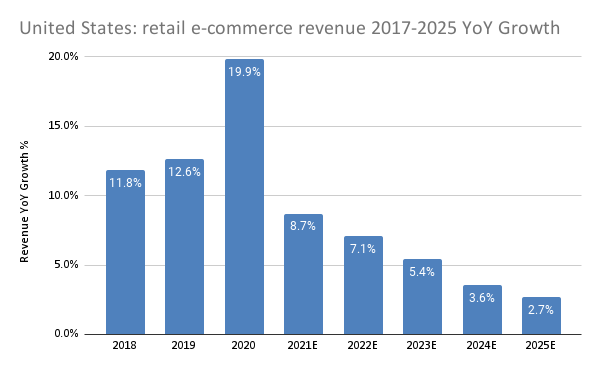

We could see from the above why ramping up growth internationally is so important for Shopify to continue delivering its expected spectacular growth rates. Even though Shopify merchants sell internationally, the fact that the SFN currently serves only businesses whosell to U.S. customersindicates the significance of the U.S. consumers to Shopify’s ecommerce revenues. However, as the growth of U.S. retail e-commerce revenue is expected to slow down over time (from 8.7% YoY in 2021 to 2.7% YoY by 2025), companies like Shopify who rely on high growth to justify its valuation must either take market share away from its key competitors or look for growth outside of the United States.

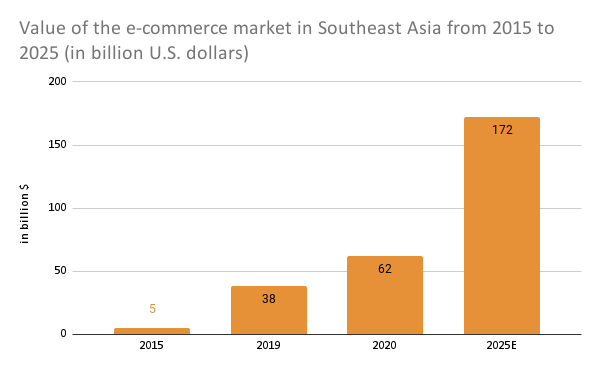

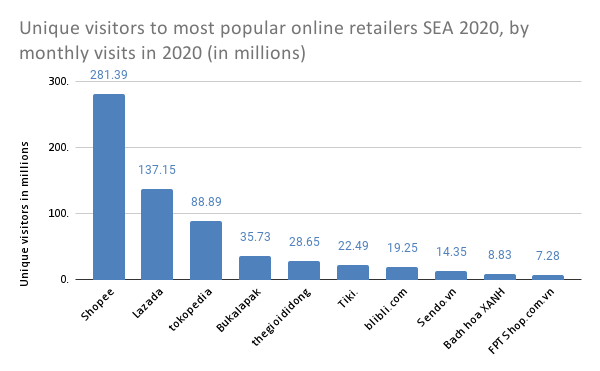

For example, if we look across to Southeast Asia, and compare the growth rates of the Southeast Asian market (expected 5Y CAGR for 2020 to 2025: 22.6%) and the United States market (expected 5Y CAGR for 2020 to 2025: 3.73%), it’s easy to see which market will be the key driver of e-commerce growth in the near future. There’s no doubt that the U.S. market remains an extremely important market given its size, however much of the future growth will likely come from overseas markets. Therefore, it’s important that Shopify continues to drive growth across other geographical markets.

Let's Bring in Sea Limited

In order to look at Shopify’s growth opportunities in the Southeast Asian market, I thought it would be important to first consider the most important e-commerce player in that region: Sea Limited (SE), which I had previouslycovered in detail in an article hererecently.

It’s easy to see how SHOP’s more profitable business model on relying on subscriptions and merchant solutions drove a much higher EBIT margin as compared to SE’s online marketplace platform: Shopee, which is currently being supported by the company’s profitable Garena gaming segment.

Despite that, Sea has still been able to drive significant revenue growth and operating efficiencies such that its EBIT margins have seen remarkable improvement.

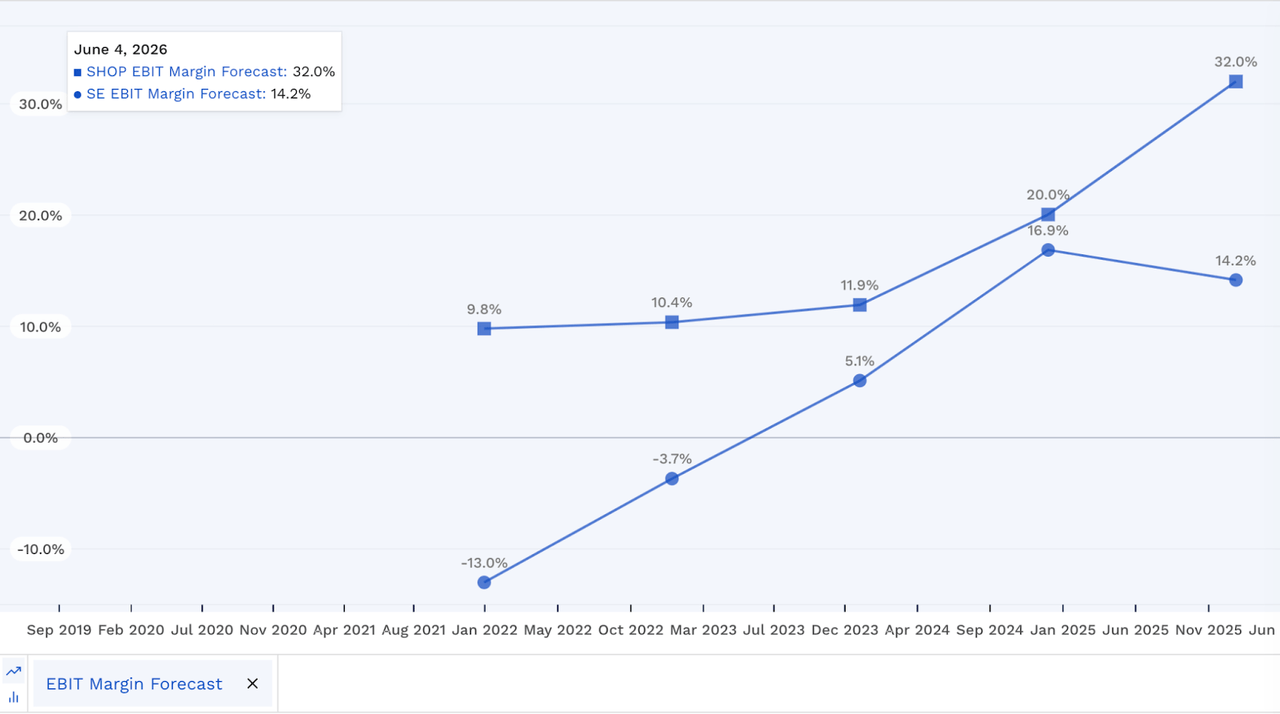

When we modelled SE and SHOP’s EBIT margins moving forward, we could see how both companies’ improving cost efficiencies, notably from the reduction in SG&A margins, would help both companies to continue improving their operating margins over time.

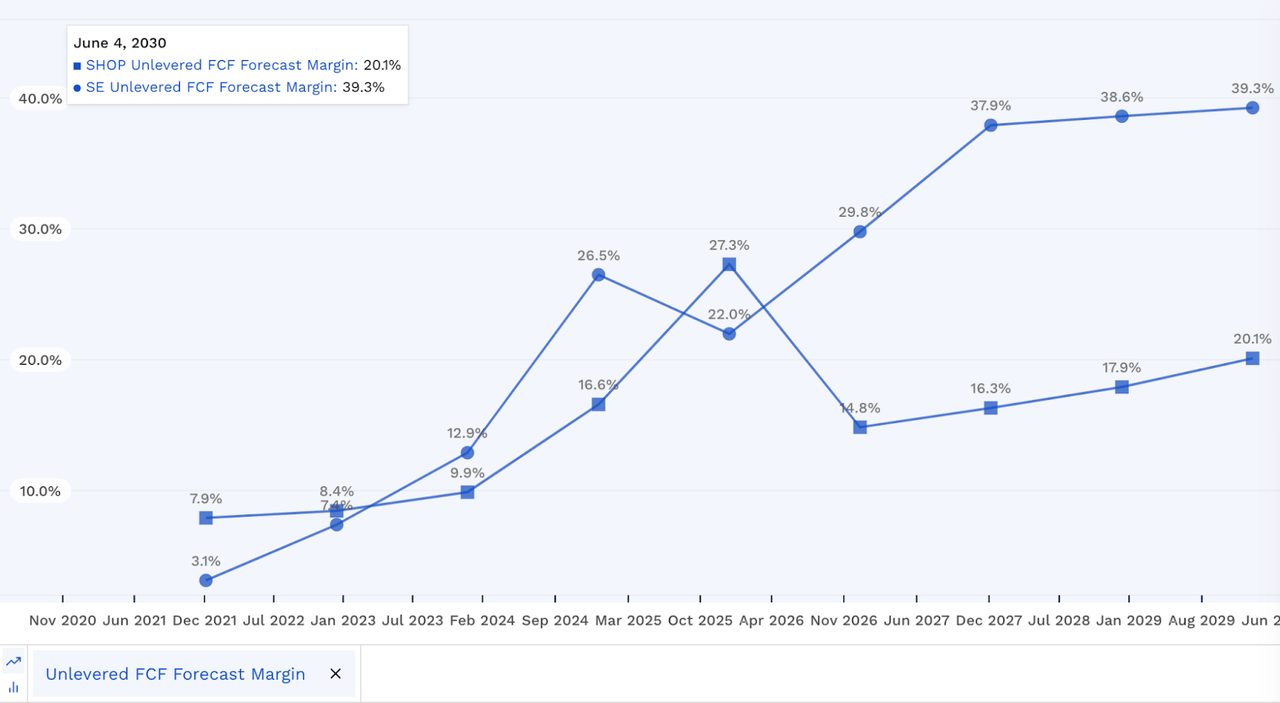

This is where their SE is expected to pull ahead. In modelling their FCF, SE is expected to generate so much FCF from its revenue growth and operating profits that the company looks increasingly like a massive cash flow machine moving forward. It’s not as if SHOP looks sloppy, but when compared to SE’s FCF margins, they certainly don’t look as impressive though.

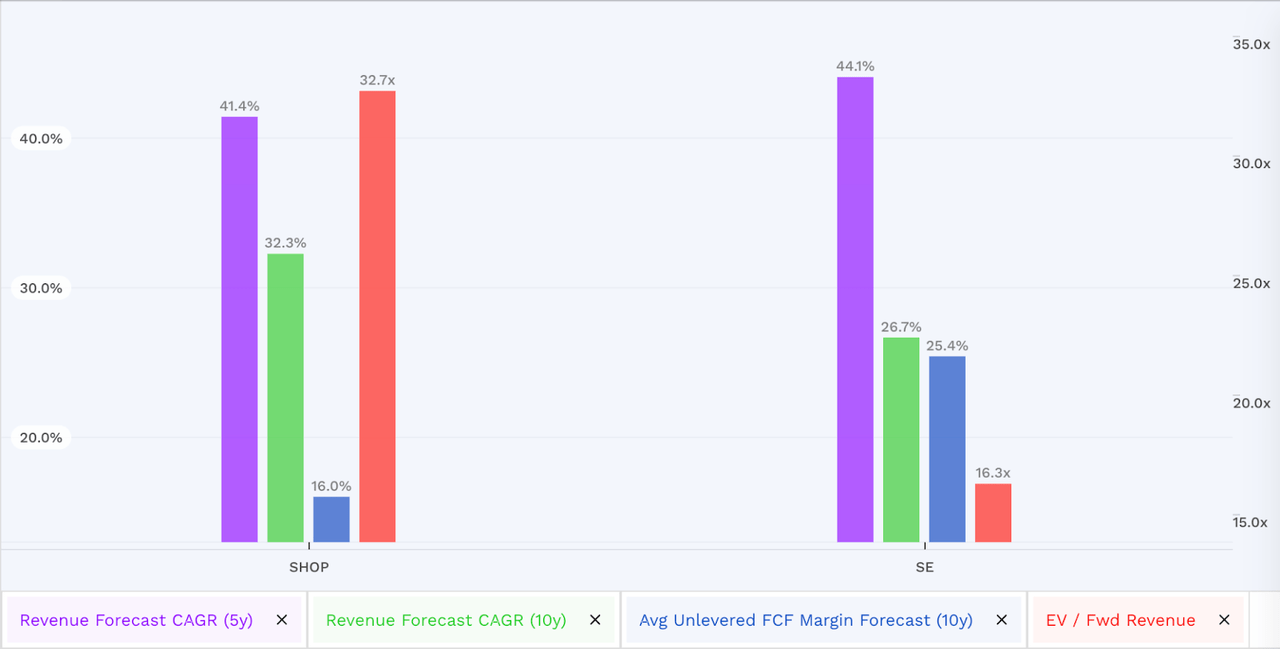

More importantly, when we bring their current valuation levels into the picture (EV / FY+1 Rev), we could see that SE’s current valuation (16.3x) looks so much more attractive than SHOP’s (32.7x), while being able to convert that rapid revenue growth into higher FCF margins. It should also be noted that I have modelled both companies to continue their blockbuster performances: SE (5Y CAGR of 44.3%, 10Y CAGR of 26.7%), SHOP (5Y CAGR 41.4%, 10Y CAGR 32.3%).

Therefore, for investors who would like a share of that rapid international growth in the Southeast Asian market coupled with a leading cash flow generating gaming segment, you should look no further than SE.

When we consider the competitive economics in the U.S. against Southeast Asia, it becomes very clear. Shopify faces strong competition within its software platform segment, without accounting for Amazon’s prowess as well. Even though I expect Shopify to continue its rapid expansion, I believe that it faces more intensive competitive threats than Sea Limited as the pie in the U.S. is expected to grow slower over time. SHOP needs almost perfect execution every quarter to justify its lofty valuations.

As compared to SE, it is clearly the dominant online marketplace now in Southeast Asia by a fairly large margin, and its prowess and scale is also growing, further stretching the distance from its competitors. Coupled with its ShopeePay payments platform, it also creates a flywheel effect similar to what Shopify Payments does for Shopify. The leadership in Southeast Asia is surely Sea’s to lose, and there’s so much potential growth that the company can capture in this region as the undisputed leader. When we consider Shopify’s valuations against SE’s it looks quite clear SE’s valuation looks more attractive now, with stronger market leadership and arguably higher potential growth.

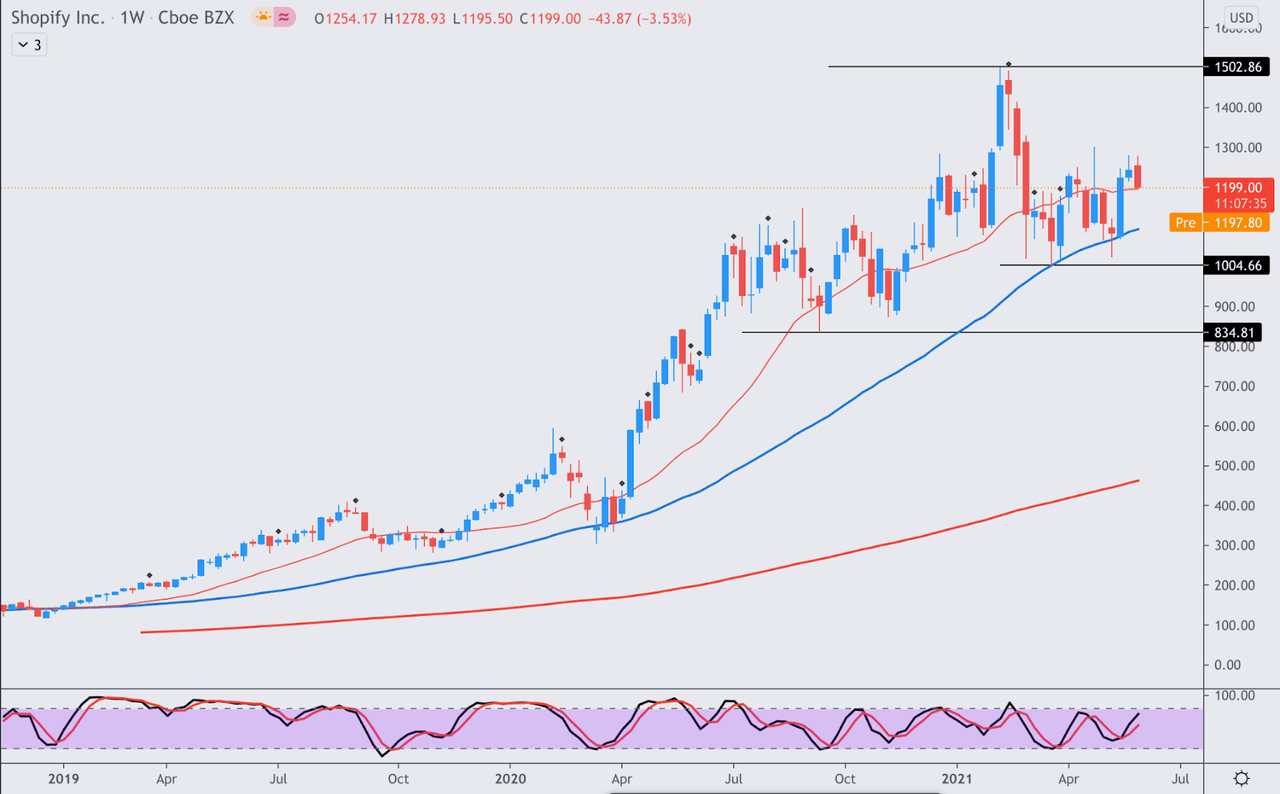

Price Action and Technical Analysis

SHOP’s price action has been stuck somewhat in a large consolidation phase since Oct 20, with the bull trap set in Feb 21 at around the $1500 level. Support was found at around the $1000 level, with further support at around the $835 level for investors who wish to add further into SHOP. It’s important to note that despite SHOP’s lofty valuations, its long term uptrend bias has never been threatened, and I expect this to carry on moving forward.

Wrapping it all up

Although Shopify is one of the most expensive high quality e-commerce stocks right now, it’s also expected to generate rapid growth ahead with its ever improving ecosystem for its merchants. Coupled with one of the strongest long term uptrend biases that I have seen for stocks (It didn’t lose its key support levels even during the COVID-19 bear market), I believe this puts SHOP in a strong position as a stock to add aggressively at the next big dip.