Summary

- Cloudflare is a high-performance CDN. Its paying customers continue to rapidly increase and show no signs of slowing down.

- Cloudflare's gross margins are very high, reaching the high 70s%.

- Cloudflare is priced at 53x forward sales, making it one of the most expensive SaaS names.

Investment Thesis

Cloudflare(NYSE:NET)is Content Delivery Network (''CDN''). As the world continues to rapidly digitize, the demand for high-quality and fast internet networks continues to increase. To this end, it's perhaps no surprise that investors have long ago understood these prospects and reflected this belief into Cloudflare's share price. In fact, Cloudflare is now priced at 53x forward sales making it one of the most expensive SaaS names.

Having said that, Cloudflare's growth rates continue to be persistently high and stable. Investors interested in Cloudflare will have to adopt a firm buy-and-hold strategy.

Voting Machine vs Weighing Machine

Cloudflare is a Content Delivery Network (''CDN''). Its mission is to make the internet secure, faster, and more reliable.

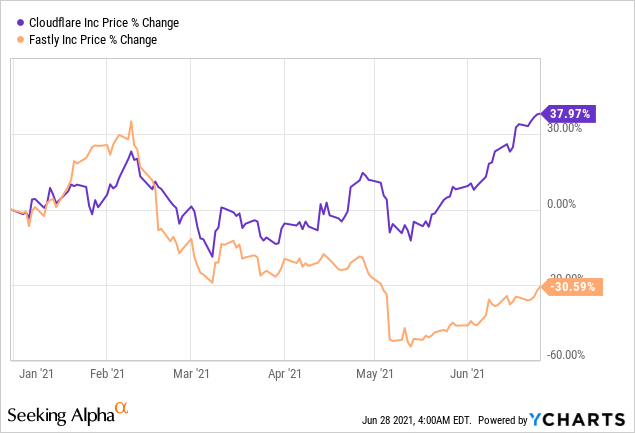

This time last year, investors were passionately clamoring for Fastly (FSLY). It was viewed by many as a company that could do no wrong. This year, it's a dramatically different setup as the graph above depicts. Fastly has fallen by the wayside, while Cloudflare is now the reigning champion.

Investors are voting with their feet to exit Fastly and they are now piling in around Cloudflare.

As a value investor, I would normally argue that this is likely to once again revert. Here is a quote from Horace that legendary investor Benjamin Graham's investment philosophy was based on:many shall berestoredthat now are fallen and many shall fall that now are in honor.

Having said that, for every snapping one-liner an investor might put out, the real investor's prospects lie in doing the work and attempting to discern the underlying opportunity.

Cloudflare is a High-Quality Business

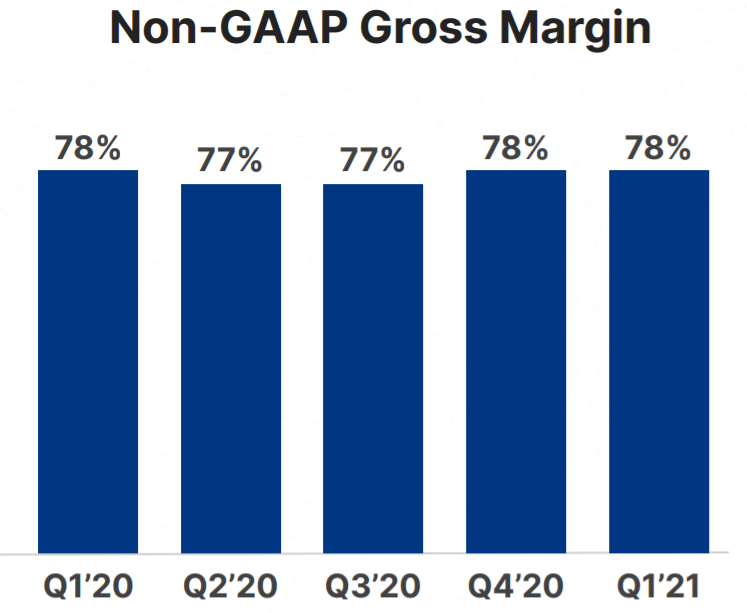

Cloudflare's non-GAAP gross margins are not only incredibly high, but they are highly stable too.

As a reminder, this compares with Fastly's60.1%as of Q1 2021. On the surface, this is incredibly alluring and is a typical indicator of a high-quality business.

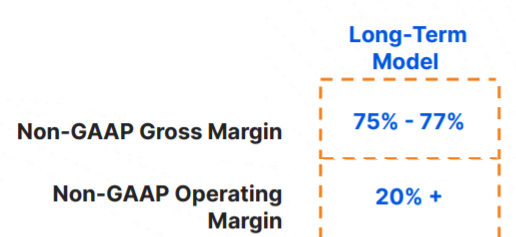

On the other hand, as we look out to Cloudflare's full-year guidance, its non-GAAP operating margins are expected to come in ata negative 4%. Of course, this is a substantial improvement from the negative 8% from 2020 and puts Cloudflare very close to breakeven.

Nevertheless, to go fromnegative 4% to positive +20% in operating margins is a very steep climb. So, investors should be cautious and take this guide with a pinch of salt.

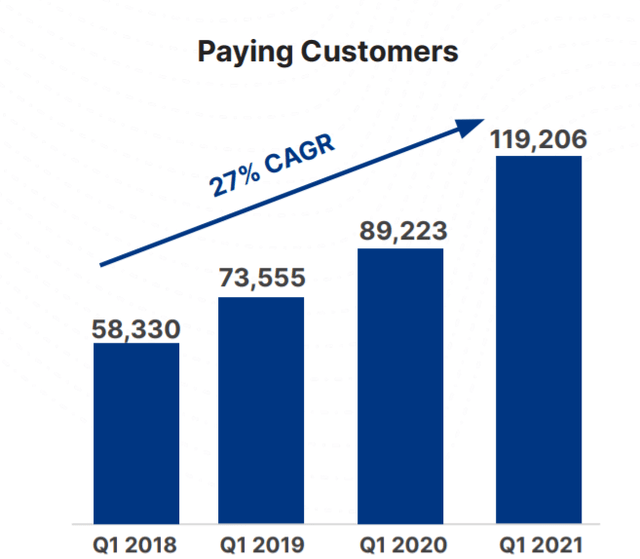

Moving on, its latest sets of results put Cloudflare's dollar-based net retention at 123%. This is an important metric because it not only shows that the company's customer base is sticky but reminds us that Cloudflare is capable of upselling 23% more services to its customers y/y.

This insight, together with the fact that Cloudflare's paying customers continue to increase, should provide investors with confidence that Cloudflare's business is very healthy, as its revenues are increasing by a mixture of increasing customers and higher prices:

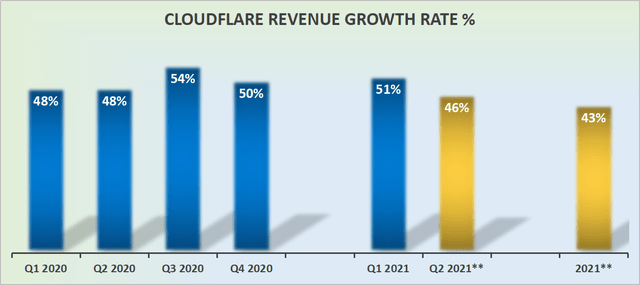

Revenue Growth Rates: Strong and Stable

Next, we can see above that Cloudflare continues to guide investors for mid-40s% CAGR - at least in the near term.

Furthermore, knowing how conservative this management is, I suspect that Cloudflare will easily beat these targets and will perhaps even raise its guidance over the coming year.

Nonetheless, we have to keep in mind that we are still discussing a company that's likely to finish 2021 with close to $600 million in revenues. In other words, growing at mid 40s% while the company is at sub $1 billion in revenues, and continuing to grow at mid-40s% at higher than $1 billion in revenues, it's quite a different feat. At some point, size takes a toll.

Valuation - Not Cheap

Cloudflare is priced at 53x forward sales. This implies that optimism towards Cloudflare is incredibly high. Even amongst SaaS names, I believe this is an outlier. I follow many companies in this space and I don't know of any that are priced as richly as this.

The obvious comparison here is Fastly which is priced at 18x forward sales. But even amongst the cybersecurity names, a sector that is wildly known for its exuberant valuations the likes of CrowdStrike (CRWD) is priced at 42x sales.

The Bottom Line

Cloudflare is remarkably stable and growing at a rapid rate. Its valuation is not cheap at 53x sales, but there again high-quality companies rarely are. Investors intent on taking a position here may consider buying in dips.

Having said that, I prefer to stick to companies with more hairs on them and more cheaply valued. Happy investing!