Summary

- ASML is supplying the critical extreme ultraviolet lithography machines for the leading-edge foundries. It has no competitors in this market.

- Investors have been willing to pay up for its dominance in this market.

- However, its current valuation looks stretched, as growth is expected to slow.

- We discuss why we think investors should wait for a deeper retracement first before considering adding exposure.

Investment Thesis

ASML Holding N.V. (ASML) is one of the leading players in the wafer fabrication equipment (WFE) market. As the only player capable of manufacturing extreme ultraviolet (EUV) lithography machines, ASML has no competitors in this category. Taiwan Semiconductor (TSM), Samsung (OTC:SSNLF), and Intel (INTC) have to depend on ASML to supply these highly coveted and costly machines. In addition, the secular demand drivers underpinning the 5G ramp, IoT, autonomous vehicles, and high-performance computing will continue to benefit ASML EUV demand.

ASML also telegraphed a backlog that amounted to EUR 19.6B in FQ3, including EUR 11.6B in EUV. Consequently, it has given them revenue visibility until early 2023, as the company continues to add capacity.

Nevertheless, we believe that a significant amount of growth premium has been baked into the stock's current valuation. It leaves little margin for error and would require ASML to execute immaculately. While we do not question management's ability to execute, we are also concerned about the potential or a correction due to excess capacity from 2023/24 onwards.

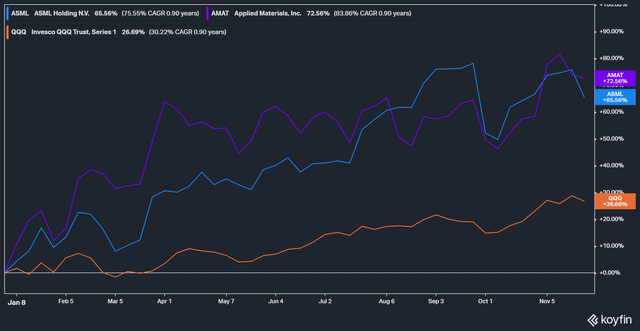

ASML Stock YTD Performance

It has been a fabulous year for ASML investors. The stock's momentum has been robust all year as it rode the secular drivers underpinning its industry. Moreover, given its dominance in EUV lithography, investors are willing to continue paying up to own its shares. As a result, ASML stock's YTD gain of 65.6% easily outperformed the Invesco QQQ ETF's (QQQ) YTD return of 26.7%. However, its WFE rival Applied Materials (AMAT) stock is slightly ahead with a YTD gain of 72.5%.

A Strong 2021 for ASML. What about its Prognosis Moving Forward?

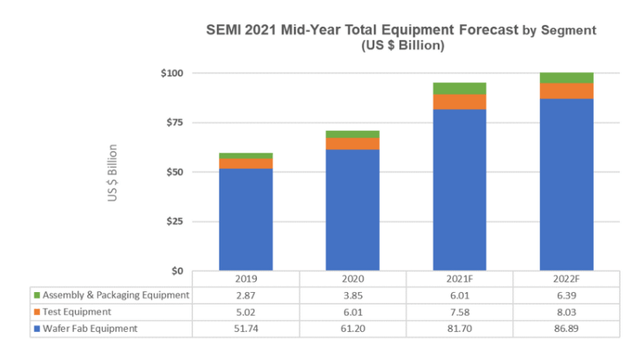

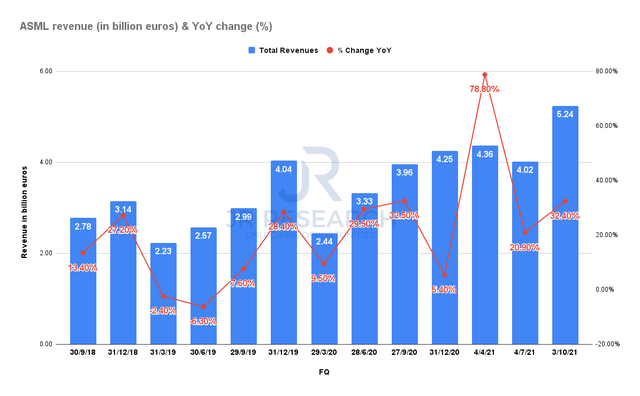

It has been a banner year for the semiconductor industry and the WFE market. SEMI estimated that WFE sales would increase by 33.5% YoY in 2021. ASML guided for its revenue to grow by 35% YoY in FY21. Given the company's solid performance in FQ1-FQ3 so far, we believe that ASML's guidance is highly credible. It's also well in line with the industry's forecasts, so it's highly reasonable as well. Despite the supply chain problems that ASML is facing, it still expects a robust FQ4, guiding for revenue of between EUR 4.9B to EUR 5.2B. CEO Peter Wennink emphasized (edited):

We're seeing continued strong demand from our customers across all market segmentsfrom both advanced and mature nodes, driving demand across our entire product portfolio. These end market trends are driving strong demand across all market segments and across our entire technology portfolio. Therefore, we continue to increase our capacityfor all of our products to meet customer capacity and technology requirements. (from ASML's FQ3'21 earnings call)

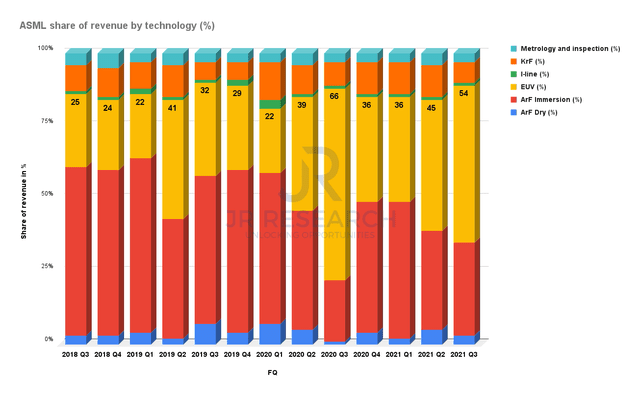

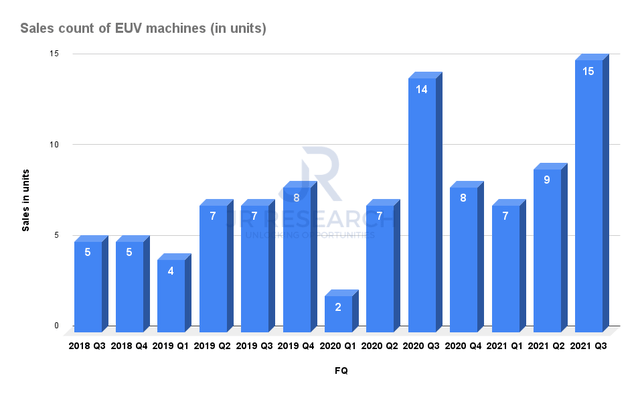

EUV has driven sales for ASML tremendously over the last three years. We can easily glean from the growth cadence of the unit sales, and EUV's share of the revenue. In FQ3, EUV's share of revenue remains influential and consistent at 54%. In addition, its foundry customers have telegraphed their plans to increase CapEx intensity moving forward to support robust underlying demand. Therefore, we believe EUV's share of revenue will remain robust.

Nevertheless, it's also important to note that its DUV systems are critical in driving ASML's revenue. Hence, while the secular demand underpinning EUV's strength is commendable, the concern of overcapacity has been widely discussed along the mature nodes.

TSMC CEO C.C. Wei also discussed the possibility of an "inventory correction" moving forward. He articulated:

Let me say that while we do not rule out the possibility of an inventory correction, but we expect TSMC's capacity remain very tight in 2021 and throughout 2022. This is because of our technology leadership position. And even there's a correction to occur, we believe it could be less volatile for TSMC than previous downturn due to our underlying structural megatrend of 5G-related and HPC applications. (from TSMC's FQ3'21 earnings call)

Hence, TSM recognizes that the potential for excess capacity could affect the trailing nodes much more than leading nodes. However, TSM's CapEx is heavily focused on the leading-edge, as it accounted for 80% of its CapEx investments. Therefore, a potential downturn is less likely to hit the foundry leader significantly.

In addition, the problems could intensify in the automotive market. TSMC emphasized that it discovered that the automotive supply chain is very complex and challenging to grasp well. CEO C.C. Wei emphasized: "Let me specifically point it out. The automotive supply chain actually is quite long and complex. It's more complicated than we initially thought."

Even ASML had cautioned that it has also been unable to fully understand the bottlenecks in the supply chain. While the company has attempted its best to model and survey, it hasn't found a viable answer. In response to an analyst's question on the source of the supply bottlenecks, CEO Peter Wennink accentuated (edited):

So -- and the real answer is we don't know. Because somehow we haven't been able to connect all the dots that actually are the underlying drivers for this demand. There's some rumors out there that the brokers and the distributors are stocking up all the inventory to drive up the prices. I know one thing that the demand for mature, for DUV dry has by far exceeded our expectations. Some of it will be panic ordering by the customers of our customers. But it's too big to just be panic ordering. So there is this underlying trend that we really don't understand fully.(from ASML's FQ3'21 earnings call)

So, is ASML Stock a Buy Now?

Much has been said about ASML's dominance in leading-edge EUV systems and how it will continue to entrench its leadership. But, it may be helpful for investors to remember that its mature nodes systems also drive the company's stock valuation.

Mordor Intelligence estimates that the EUV market would grow by a CAGR of 15% from 2020 to 2026. Considering ASML's FY21 guidance of 35% YoY growth, ASML expects slower growth ahead even with the capacity ramp. Wennink also suggested that corrections cannot be ruled out, even though he emphasized that it's unlikely to happen soon. He mentioned (edited):

Yes. I mean, we have corrections. We have always seen corrections in our industry. I'm not going to say that they're not there. But we have to look at some of the trends that we're also seeing. And we look at the announcement of the build-out of new capacity. Just refer to the US chip sector, EUR 52 billion, of which EUR 40 billion is for basically to support expansion of capacity. That's going to happen over the next couple of years. It will take 2 to 3 years. So when will this inevitable correction come, I don't think it's likely to come anywhere soon. (from ASML's FQ3'21 earnings call)

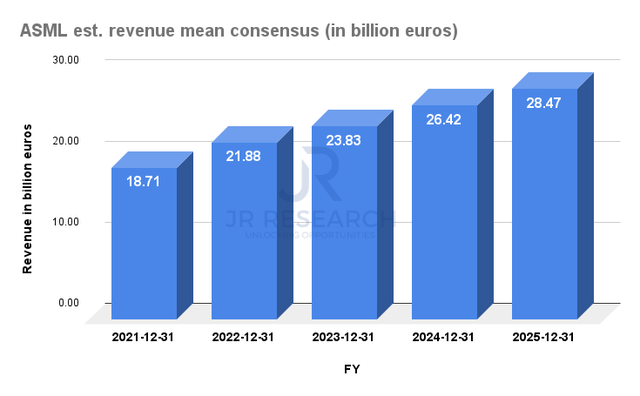

We applaud management for having the confidence to issue long-term guidance of 11% CAGR from 2020 to 2030. Management also provided revenue visibility till FY25, as it expected revenue of between EUR 24B and EUR 30B. Consensus estimates point to revenue of EUR 28.5B, which is at the higher end of ASML's mid-term guidance. Therefore, consensus estimates imply a revenue CAGR of 11.1% over the next four years, aligning with ASML's long-term guidance. Notably, it's also in line with Mordor Intelligence's estimates from FY20. ASML is projected to grow its revenue at a CAGR of 15.3% from FY20 to FY26. Hence, we are confident that the company's revenue guidance and the consensus estimates are well-aligned and credible.

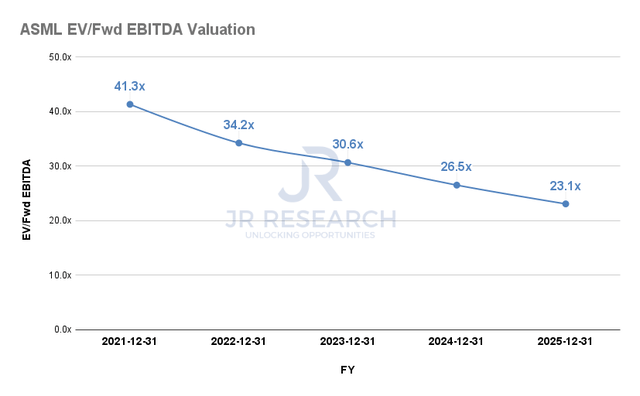

We believe the clear revenue runway ahead for ASML has given investors confidence to continue paying a premium for ASML stock. The stock is currently trading at an EV/NTM EBITDA of 35.3x, 31.2% above its 3Y mean of 26.9x.

However, ASML stock has found support whenever its NTM EBITDA multiple reached about 32.3x in 2021. The stock is trading at about 9.3% above this support level. Despite that, we are cautious about paying such a high premium for a stock where we consider at least two to three years of EBITDA growth could have been priced in.

There is little doubt that ASML stock is a high-quality stock with a clear revenue runway. But, we are careful about paying the current premium asked. Therefore, we encourage investors to wait for a deeper retracement for a safer entry point.

Consequently, werate ASML at Neutral for now. But we may consider adding exposure if we observe a meaningful retracement.

Written by JR Research