The cybersecurity specialist is showing signs of stepping on the gas.

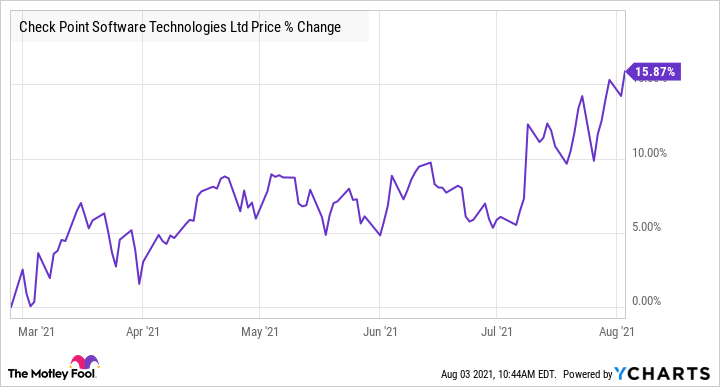

Check Point may not be one of the most fashionable names in the cybersecurity industry, but the stock has been gradually gaining some momentum on the market since the beginning of March.

Known for following a slow and steady approach in an industry where its rivals have been growing at a breakneck pace, Check Point's recent stock price rally isn't surprising as it has beensshowing signs of switching into a higher gear. The company's second-quarter results provide further indication that Check Point's rally could get stronger, as it seems to be pulling the right strings to step on the gas in the future.

Let's look at the company's latest numbers and see why this might be a cybersecurity stock worth buying.

A closer look at Check Point's latest quarter

Check Point's revenue increased 4% year over year in Q2 to $526 million, while non-GAAP earnings increased just 2% to $1.61 per share. Wall Street expected the company to deliver $1.56 per share in earnings on $523.8 million in revenue. Admittedly, Check Point's year-over-year growth was nothing to write home about.

the company's guidance didn't do much to turn heads either. Management expects third-quarter revenue between $515 million and $540 million. Adjusted earnings are expected to fall between $1.54 and $1.64 per share. Check Point had delivered $1.64 per share in earnings in the prior-year period on revenue of $509 million.

So, while the company's revenue could grow in low single-digit percentages year over year, its earnings are on track to shrink.

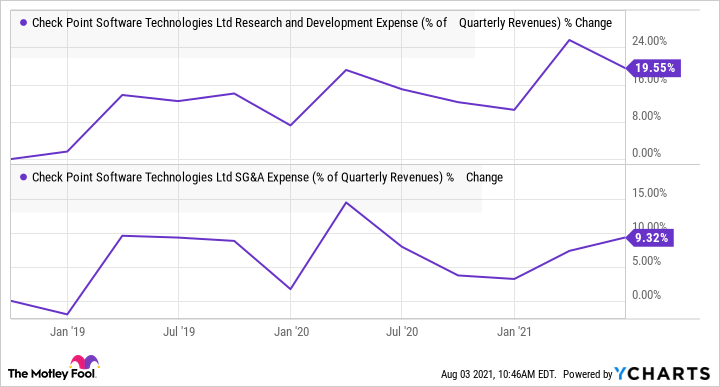

However, investors shouldn't read too much into the shrinking bottom-line performance. That's because Check Point has been conservative over the years when spending money. The cybersecurity specialist's spending on research and development (R&D) and marketing has lagged behind its rivals. While that has made Check Point a profitable cybersecurity company, its slow pace of revenue growth shows that it is missing out on the terrific growth that the industry offers.

The good news is that Check Point has been breaking away from that trend of late.

Check Point spent 41.1% of its revenue on R&D and marketing last quarter, up from 40.1% in the year-ago period. While that's not a huge increase, it is worth noting that Check Point's new strategy of spending more money in the cutthroat cybersecurity market is reaping results and paving the way for long-term growth.

Gearing up for long-term growth

Check Point's deferred revenueincreased 10% year over year in Q2 to $1.47 billion, substantially outpacing the actual revenue growth. That's a nice bump over the year-ago period's deferred revenue increase of just 4%.

The acceleration in the company's deferred revenue growth is good news for investors, as the metric refers to the money collected in advance in lieu of services that will be rendered at a later date. The deferred revenue is recognized on the income statement once the services are actually delivered, indicating that Check Point's subscription business is gathering momentum.

Check Point's revenue from security subscription sales jumped 12% year over year to $183.7 million, accounting for nearly 35% of the top line. The segment had produced 32.4% of Check Point's total revenue in the prior year period. The software updates and maintenance business also recorded a 2% year-over-year increase.

However, the legacy products and licenses business that accounts for 22.6% of the company's revenue was a laggard. The segment's revenue fell nearly 3% year over year, a trend that's likely to continue as Check Point focuses more on the subscription side of the business where it is witnessing impressive traction.

CloudGuard and Harmony -- Check Point's offerings for the cloud security and secure access markets -- now account for 20% of its security subscription revenue. What's more, the revenue from these two product lines has doubled in the past two years. The revenue from Check Point's Infinity architecture, which combines CloudGuard, Harmony, and the Quantum network security solution, has tripled since the beginning of last year.

All of this indicates that Check Point is steadily working toward a high-growth revenue model that could help the stock deliver upside in the long run. That's why investors looking to add a long-term cybersecurity play to their portfolios should take a closer look at Check Point. It is trading at 20.7 times trailing earnings, which is a discount to the stock's five-year average multiple of 21.7.