A shocking week on the inflation front has left a dent in stocks, with major indexes set to deliver 1%-plus losses across the board. That’s even as some Wall Street strategists see little blocking further stock gains or that frequent year-end melt-up.

Yet the worry festers, such as for Nicolai Tangen, the manager of Norways’ $1.4 trillion sovereign-wealth fund, the biggest money pot in the world.

“We’re looking at the degree of euphoria. With markets really panicky last year, we have entered a very euphoric phase, and we just need to consistently gauge the levels of euphoria,” Tangen said in a recent interview with Devin Banerjee, editor at large, business and finance for LinkedIn.

“And then, of course, the real threat is inflation. If inflation really takes off, that’s going to be bad news both for our bond portfolio and for the equity portfolio. So, that’s where we have the laser focus,” added Tangen.

It’s a reminder that what some see as heady times for stocks aren’t going unnoticed.

That brings us to our call of the day from Michael O’Rourke, chief market strategist at JonesTrading, who falls into that camp with his latest note entitled “In case there are bubble doubts.”

He writes: “Since the U.S. financial markets have achieved new levels of insanity, we want to make sure we document this moment in time for posterity’s sake. Apparently, we have not learned anything from the Equity, Housing and Credit bubbles that occurred between 1999 and 2008.

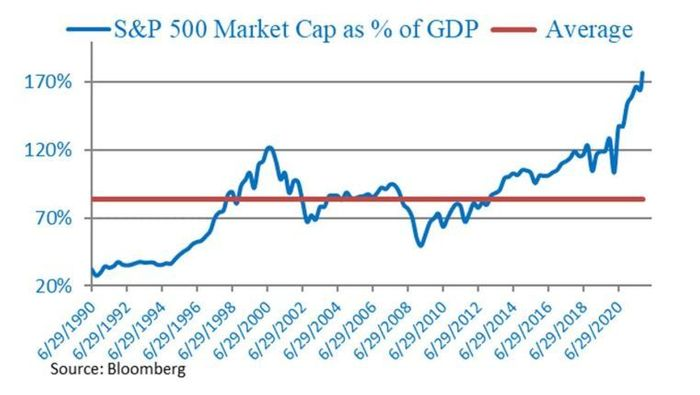

“It can’t be any clearer than the fact that the S&P 500’s market capitalization is 177% of U.S. GDP,” adds O’Rourke, who provides this chart:

During the 2000 tech bubble, the S&P 500’s market capitalization peaked at 121% of nominal gross domestic product, he says.

“That should paint a stark picture as to how expensive today’s market is relative to the last generational equity bubble,” says O’Rourke, who adds that the current level is also double the average reading of the past three decades and triple the valuation where the S&P 500 bottomed during the 2008-09 financial crisis.

“Even with the greater inflationary bump to Nominal GDP, it would need to grow at 8% for a decade to return to the historic market cap to GDP average,” he says.

“The $3 trillion in crypto (whose only purpose appears to be speculation) is a clear illustration of an environment that knows no fear. Nonetheless, we are among the few who fear a 50% S&P 500 valuation drop that would bring the index’s market capitalization back in line with its average historic relationship to GDP,” he says.

O’Rourke reminds of us a “painful” 80% decline for the Nasdaq Composite between March 2000 and October 2002. “Just think, the broad tape is 50% more expensive today than March 2000,” he says.

Back then, Amazon was a top internet company and highly regarded stock, but shares still slumped 95% between December 1999 and September 2001, he says.

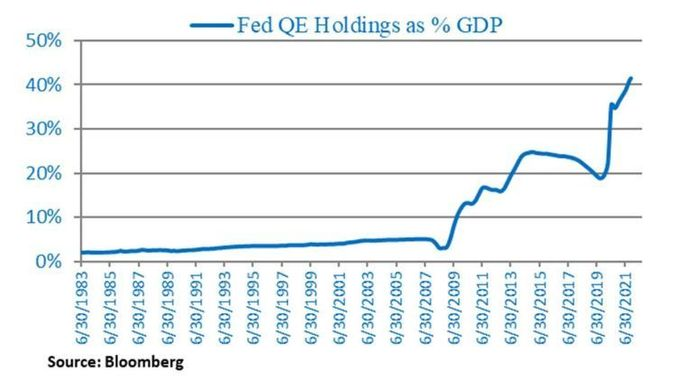

The strategist goes on to point the finger at the Federal Reserve and other central banks for propping up markets. “Today, the world is no better than the one two decades ago, and it is arguably worse. It is simply that these extra trillions of dollars having entered the economy in a short period of time provide the pretense of a special time meriting unsustainable valuations,” he says.